How Far Can Big Discount Supermarkets Expand?

UK - Lessons from France and Germany can show us the future of supermarkets such as Aldi and Lidl, say analysts from BPEX. 7 April 2015

7 April 2015

3 minute read

3 minute read

By:

By: Aldi and Lidl continue to increase market share as mainstream supermarkets contract - the question is how far can they go? Operating across a narrow product range, the hard discounters rely on enticing an ever greater proportion of mainstream shoppers into their stores to gain market share.

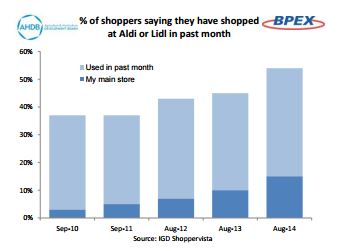

In GB, it is only in the last five years that Aldi and Lidl have been successful in going mainstream – with 54 per cent of shoppers from across the socioeconomic spectrum using these stores at least once a month according to IGD.

According to Kantar data, Aldi and Lidl now together account for 8 per cent of the GB market.

While it is impossible to accurately quantify the future growth of hard discounters in GB, there are some indications of what trajectory discounter growth might take from trends in other EU countries.

In their home market, Germany, discounters such as Aldi and Lidl together account for around 37 per cent of the grocery market share with 85 per cent of all shoppers using Aldi at least once a year. Here discounter growth has stalled for a number of years, despite less market competition from large multiple retailers compared to GB, suggesting a natural growth ceiling.

In France, mainstream supermarkets have fought back and hard discounters have declined. Here, the discounters reached a similar market share to GB (8 per cent) in 1998.

Growth continued to reach 14 per cent in 2009, when the proportion of shoppers using them reached 73 per cent.

French supermarkets reacted by becoming price competitive with discounters, expanding budget lines, moving away from promotions to everyday low pricing and redefining own-label tiers around clear quality and value-for-money price points.

Without a strong price advantage, hard discounters have been losing market share year on year since 2009 and now account for just 12 per cent. In this period, hard discounters in France have lost 1.2 million customers and have recently closed 150 stores.

GB is a tough market for the discounters and most retail market analysts do not foresee them reaching a similar market share to Germany. They do predict that discounters could achieve a share of between 15 per cent and 20 per cent, as has already happened in Ireland.

In terms of speed of growth, according to retail analysts, the UK will be the fastest growing European market for hard discounters, growing at an 11 per cent compound annual growth rate between 2013 and 2018.

This prediction is underpinned by rapid investment and expansion plans. Aldi plans a 67 per cent expansion to 1,000 outlets by 2022.

Meanwhile, Lidl has long-term plans to more than double its number of stores in the UK to around 1,500.

In lessons learnt from experience in Germany and France, hard discounters are now looking to also grow share by increasing average shopper spend through trading up. They are achieving this by working with a select number of brand leaders and adding premium quality tiers to their privatelabel fresh product ranges.

Aldi, in particular, has seen an opportunity to expand its premium British sourced fresh produce offering - meat, dairy products, fruit and vegetables with some stores opening in-store bakeries. The discounter now stocks a range of organic fruit and vegetables as well as speciality meat cuts and dairy products.

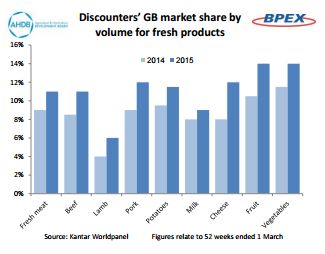

Latest 52-week Kantar data shows that Aldi and Lidl have strong growth rates and are overtrading in these categories at a time when the overall market volumes are static or in decline.

Meanwhile, there are some clear boundaries in terms of where discounters can develop further share. It is unclear how far discounters can go in their quest to mimic the large multiples before diluting the strength of their low cost model.

They have no share of the growing online grocery channel and risk losing share to other discounters if they move too far away from their original credentials.

Also, in similarities to France, mainstream GB retailers are increasingly responding to the threat of future discounter growth. Morrisons have launched ‘Match and More’ and Tesco and Asda have reduced prices on everyday product lines.

However, it is unclear how far large multiple retailers can go to compete with the discounters on price without some major restructuring, as happened in France.