Japan Eases Beef Restrictions, Could Prop up Pork Prices

US - Japan’s health minister announced that the restriction on beef imports from the United States would be relaxed beginning on Friday, 1 February, to allow importation of product from cattle up to 30 months of age, writes Steve Meyer in his weekly "Market Preview" as published in National Hog Farmer magazine. 30 January 2013

30 January 2013

4 minute read

4 minute read

Exports had been limited to cattle less than 20 months old since 2005, when Japan began allowing US beef back into the country after our discovery of bovine spongiform encephalopathy (BSE) in December 2003. The restrictions had significantly limited the pool of cattle from which Japanese exports could be drawn and, in turn, created a huge opportunity for Australia to ship beef to Japan.

Japan buys some high-end beef from the United States, but a significant part of our exports there are lower value cuts, such as plate (skirt steak). Expanding the supply of cattle from which exports may be drawn will reduce the prices Japanese buyers must pay, but should result in volume growth. Any positive impact on US beef and cattle prices will, I think, have to come by the volume impact since any premiums that have been garnered for the under-20-month product will now likely be gone. I still expect this will be positive for beef prices and thus a gain for pork demand in 2013.

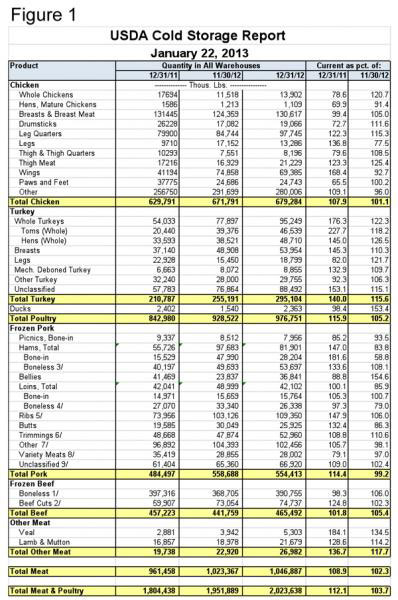

Year-End Cold Storage Stocks Up 12.1 Per Cent

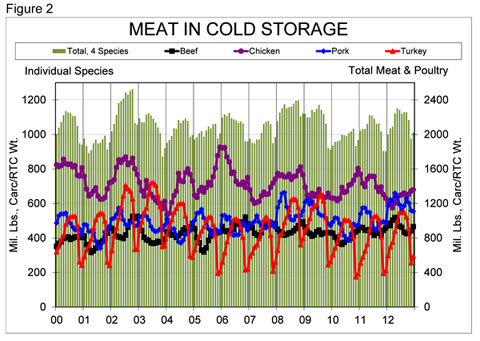

USDA’s January Cold Storage report indicates that total stocks of poultry and meat were 2.014 billion pounds on 31 December, up 12.1 per cent from one year ago and 3.7 per cent from 30 November (Figure 1). A chart of inventories by species appears in Figure 2.

Turkey: This year’s increase was led by turkey inventories which were 40 per cent larger than last year and 16 per cent larger than at the end of November, which weren’t small. In fact, typically the lowest of the year, the November stocks were the largest since 2004, except for in 2008. Whole bird stocks were the biggest factor in the growth at +76 per cent from one year ago and +22 per cent from last month. Breast stocks were down slightly from last year, but still held at 5 per cent higher than one month ago.

Pork: Pork inventories on 31 December were 14.4 per cent higher than at the same time last year but actually declined 0.8 per cent during December. There was 554.4 million pounds of pork in freezers on 31 December. For perspective, last week’s estimated pork production was 448 million pounds.

Ribs are the primary culprit in the growth of pork stocks, accounting for 50 per cent of the year-on-year increase. Ribs account for about 20 per cent of the total amount of pork in freezers and 31 December rib stocks are at a record high. The report does not indicate exactly who is holding the various inventories, but our contacts believe that a large number of these ribs are already owned by end-users. Spareribs were quoted the week of Jan. 18 at $135.59/cwt., down nearly 15 per cent from one year ago.

Chicken: Chicken stocks grew by 1.1 per cent during December and stood at 679.3 million pounds at month’s end. That is 7.9 per cent larger than one year ago. Nearly 70 million pounds of wings were in freezers on 31 December, 68 per cent larger than last year but 8 per cent fewer than last month. Wing prices are again record high in spite of these large stocks, implying exceptional demand leading up to the Super Bowl, traditionally the seasonal peak for chicken wing prices.

Chicken leg product stocks were 9 per cent larger than last year, while breast meat stocks were 0.6 per cent lower than one year ago and 5 per cent larger vs. November stocks.

Beef: Beef stocks grew by 5 per cent during December to 465.5 million pounds. That level is just 1.8 per cent larger than one year ago. However, boneless inventories, which account for the vast majority of beef in frozen storage, were 1.7 per cent lower than in 2011.

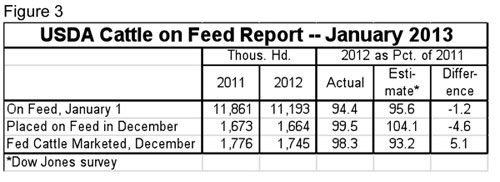

USDA’s January Cattle-on-Feed Report, released Friday afternoon (25 January), indicated significantly smaller-than-expected December placements, higher-than-expected marketings, resulting in lower-than-expected 1 January inventories. See Figure 3 for key national data.

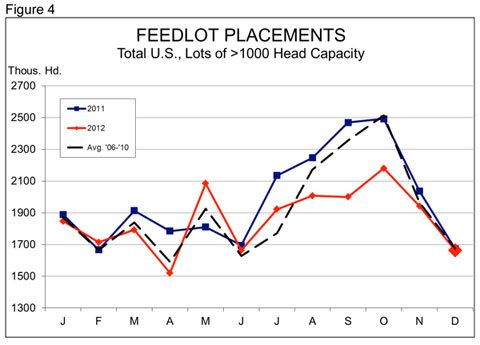

December placements of 1.664 million head were slightly lower than last year but analysts surveyed by Dow Jones before the report had, on average, expected placements to be larger than last year (Figure 4). The magnitude of the difference between the actual and expected numbers is bullish for fed cattle futures, especially for June onward.

Placements were closer to year-ago levels than they have been since the May 2011 placements were actually larger than one year earlier. Still, December marked the 10th month of 2012 in which placements were lower.

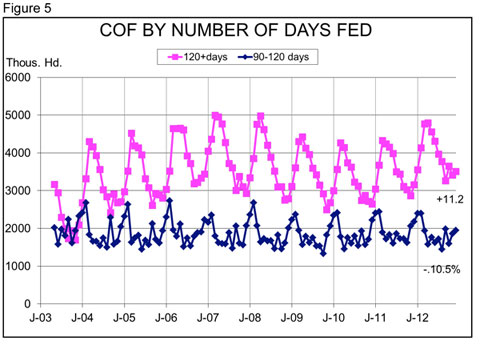

Seven straight months of year-on-year lower placements – four lower by 10 per cent or more – mean that current inventories are very front-loaded. By our calculations, there were 3.706 million cattle in lots on 1 January that had been on feed for 120 days or more. That number is 4.4 per cent larger than one year ago. But, as of 31 December, lots held 19 per cent fewer cattle (1.94 million head) that have been fed 90-120 days and 6.7 per cent fewer (5.547 million) that have been fed 90 days or less (Figure 5). Once the current supply of over 120-day cattle are gone in late February or early March, fed supplies are going to tighten a bunch.

I still expect 2013 beef slaughter to be 4-5 per cent lower than last year, but that number is very dependent on weather. If rains come to the southwest and northern plains, heifer retention will increase quickly and tighten cattle supplies in late-2013 and 2014 even further. If those rains do not materialize, there will be little for cows to eat, heifers will continue to flow to the slaughter supply and more cows will put extra product – primarily grinding beef – on the market.

All of agriculture is always dependent on weather, but have we ever seen a time when it represents such a knife edge for so many issues?