Expect Corn Projections to be Dialed Back

US - Last week, I cited two topics of concern from World Pork Expo (WPX) – Smithfield/Shuanghui and porcine epidemic diarrhea (PED) virus, writes Steve Meyer. 18 June 2013

18 June 2013

4 minute read

4 minute read

Not to be short-changed, a third concern was the impending information from the June Crop Production and World Agricultural Supply and Demand Estimate (WASDE) reports from USDA. Those were released last Wednesday. While the information in those reports is news, I suppose, little of the WASDE report differed from what we had already seen from USDA in recent months.

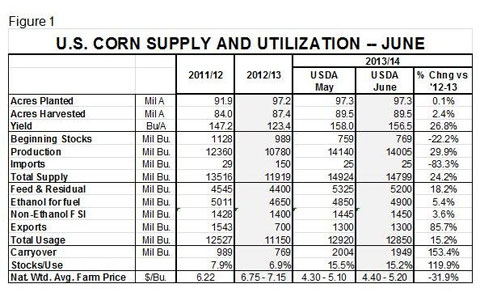

Figure 1 shows USDA’s June corn supply and utilization table from last week’s report. As expected, USDA did not change planted or harvested acre projections even though it is almost universally accepted that this year’s total will fall short of the 97.3 million acres projected in the March Prospective Plantings report.

As of last week, 95 per cent of the corn acres were planted but the percentages in some key states were substantially lower than that figure. Only 92 per cent of Iowa’s acres were planted. Minnesota plantings were at 90 per cent, while farmers in North Dakota and Wisconsin had planted only 89 per cent and 81 per cent of intended acres, respectively. Put those percentages with the planned acres and you get 1.14 million unplanted acres in Iowa, 900,000 in Minnesota, 450,000 in North Dakota and 830,000 in Wisconsin. Add in shortfalls in some other states, most notably Illinois at 490,000 acres, and last week’s progress report implies 4.5 million “unplanted” corn acres as of June 9. Some acres in Illinois, Iowa, Missouri and Indiana may still get planted, but a good portion of those Minnesota and Wisconsin and most, if not all, of the North Dakota acres are very much in doubt, especially given crop insurance features which will compensate farmers pretty well even if they plant nothing. Bottom line: The final acreage figures will be substantially lower than 97.3 million acres and could be below 94 million acres.

USDA dropped its projected yield from 158 to 156.5 bu./acre, a little more than what was expected by analysts that were surveyed before the report. But the analysts were guessing what USDA would say, not what the actual yield would be. By most accounts, that figure is much lower than 156.5 bu./acre. Iowa State’s Elwyn Taylor told WPX audiences that, according to historical yield-to-price relationships, Chicago Mercantile Exchange (CME) corn futures markets were pricing in a yield of about 147 bu./acre.

So, while the latest USDA numbers say a crop of 14.005 billion bushels, year-end 2014 stocks of 1.949 billion bushels, and, consequently, a year-end stocks-to-use ratio of 15.2 per cent, I expect we are going to see much lower numbers in July when USDA releases its upcoming acreage report and begins to earnestly estimate this year’s yield based on where the acres are and the actual condition of that crop.

If we get 94 million acres planted, harvest a normal 92 per cent of them, and get a 147-bu./acre yield, the crop will total about 12.7 billion bushels. Prices would be much higher than USDA’s current $4.40 to $5.20/bu. range, and various usages would have to be curtailed.

Total usage for 2012-13 is currently pegged at 11.15 billion bushels; 2013-14 usage would not be dialed back that far, but it could certainly be reduced to the 12.547 billion bushels of 2011-2012, implying 2014 carryout stocks of just over one billion bushels and a year-end stocks-use-ratio of 8 per cent. A similar ratio in 2011 resulted in a national average farm corn price of $6.22/bu. I thought $5.30 Dec corn futures were too high in early April. Now those futures don’t look so pricey!

Soybean Projections

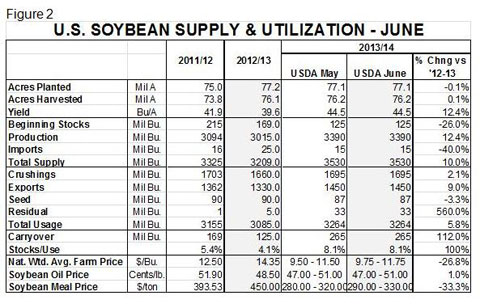

USDA made no changes at all to its 2013-2014 forecasts for soybeans except to add $10/ton to both ends of its forecast price range for soybean meal and $0.25/bu. to both ends of the range for soybeans (Figure 2). Both of those ranges are still significantly lower than current new crop futures, which are apparently quite concerned about soybean plantings and yields. Soybeans, of course, still have some growing time but the risk of an early frost is quite real, so we can understand the market’s concern.

Hog Price Prospects Better

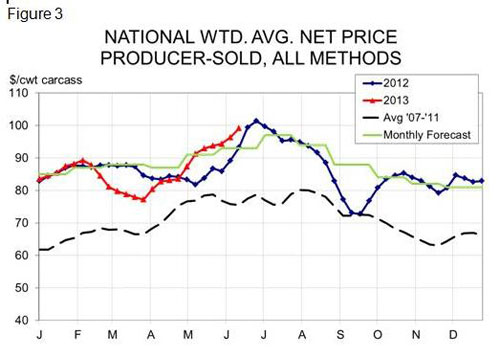

The best news of the week, of course, was the belated but much-hoped-for rally in cash hog prices and lean hog futures. Last week’s average national net hog price across all purchase methods was $99.18/cwt., the fourth-highest ever (Figure 3).

June Lean Hogs futures expired on Friday at over $102/cwt. We expect cash hogs to hang in this mid-to-upper $90s through the first part of August now that they have reached this level. Q4 hogs could be priced at about $83/cwt. on the Board of Trade which, with negative basis and positive premiums, would be near the net price received in Iowa and Minnesota; $83/cwt. is the top of my Q4 price forecast range based on the March Hogs and Pigs report, so I think producers should consider pricing some hogs at this time. It’s not a “plus-$3-over-forecast” situation in which I would say, “Sell, sell, sell!” but it is a good price relative to my expectations and taking it would reduce revenue risks significantly. Consider that reduction relative to your financial position before taking action.