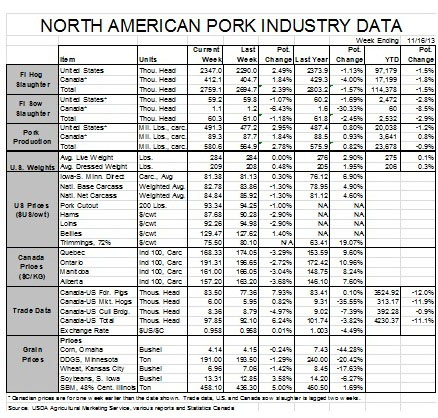

Pork Exports Continue to Struggle in September

US - US pork exports continued to struggle in September, according to data released last week by USDA’s Foreign Agricultural Service and Economic Research Service (ERS), writes Steve Meyer in his latest "Market Preview" published in National Hog Farmer magazine. 19 November 2013

19 November 2013

3 minute read

3 minute read

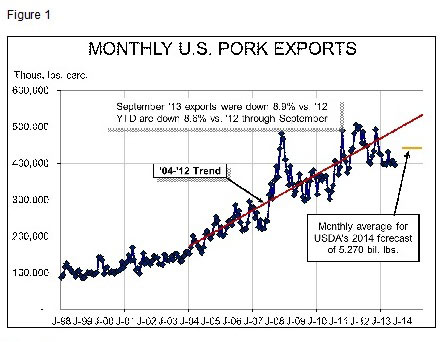

September pork exports totaled 394.9 million pounds, carcass weight equivalent. That figure is down roughly 2 per cent from August but is 8.9 per cent lower than one year ago. It brings year-to-date pork exports to 3.649 billion pounds, carcass weight, a figure 8.6 per cent lower than one year ago. September’s export figure is the lowest monthly total thus far in 2013.

Note that USDA still has higher exports in their forecast for 2014 (Figure 1). They did lower that figure from 5.31 billion pounds, carcass weight, to 5.27 billion pounds in the November World Supply and Demand Estimates (WASDE) Report, but their revised number still represents an increase of 4.3 per cent from their current annual 2013 forecast of 5.054 billion pounds.

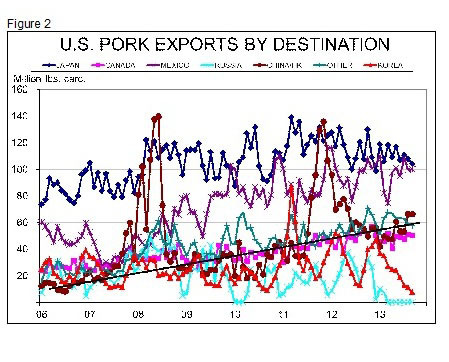

Among major markets, only Japan (+1.3 per cent) and Mexico (+1.9 per cent) have purchased more US pork this year through September. Shipments to the Caribbean and “Other” markets have grown by 35 per cent and 13 per cent this year, respectively. It should be noted that the “Other” markets used by ERS in compiling these data now account for more than 15 per cent of total US exports. So while each individual country may be small, they have a significant collective impact on our industry’s export performance.

The drivers of the lower performance are both easy to identify and familiar to pork producers and market observers – China/Hong Kong, Russia and South Korea. While exports to China/Hong Kong are significantly lower (-20.8 per cent) for 2013 to date, those markets have taken 15 per cent and 20.5 per cent, respectively, more product vs. one year ago in August and September. As can be seen in Figure 2, those values are the highest since May 2012 and represent a continuation of the long-term uptrend in exports to these markets. I still expect the Smithfield-Shuanghui deal to tilt this trend line upward in 2014 and beyond.

Shipments to Russia remain at zero with no improvement in sight. This year’s poor exports to South Korea are a bit of a mystery since we have begun to enact the Korea Free Trade Agreement. September exports to Korea were down 68 per cent from last year and bring the year-to-date total to -30.8 per cent. Tariff reductions are admittedly small so far. But one would have thought that they would have provided some stimulation to 2013 sales, especially with the Korean won strengthening slightly since June.

The only major markets to which our exports are higher this year are Japan (+1.3 per cent) and Mexico (+1.9 per cent). Those rates are obviously small but those are still our two largest volume markets so their growth is one encouraging sign.

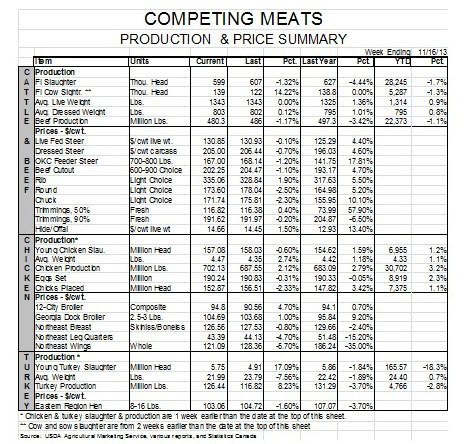

September’s muscle cut exports were valued at $413.5 million, 4.1 per cent lower than the value of August shipments and 3.3 per cent lower than one year ago. Year-to-date export value stands at $3.749 billion, 7 per cent lower than last year.

US packers/processors shipped 31.9 million pounds of pork variety meats valued at 54.336 million in September. Those figures are 10.2 per cent and 9.7 per cent lower than last year. Variety meat exports are still up 10 per cent year-to-date. The value of those higher January-September shipments is up 11.7 per cent vs. 2012.

If Russia, China and South Korea were at year-ago levels through September, our exports would be 1.8 per cent higher than one year ago.

Are there any lessons from this? I think the largest one is confirmation that the days of continuous record years are over. Our exports are now so large that increasing them year after year is very difficult and making those increases significantly large is virtually impossible. Further, many of these leading markets are large enough so that any problem will have a significant impact on the total. Finally, all of those little items that we think are not critical can become critical in a heartbeat. That is especially true for countries just looking for an excuse to protect a domestic market. And make no mistake: there are still plenty of them out there.