What's Driving Positive Pork Demand?

US - In this week's Market Preview published in National Hog Farner, Steve Meyer writes, in the past when I have posed the question “What is happening to demand?“ it has almost always been in a bad connotation. The wording would usually have better been “What the #*!):?! is happening to demand?“ You’ve been there, right? 22 January 2014

22 January 2014

4 minute read

4 minute read

Well the same question now is posed in a much more pleasant atmosphere and seeks a much more positive answer. Pork demand – and, more broadly, meat and poultry demand – has been on a roll through November, the last month for which complete data are available.

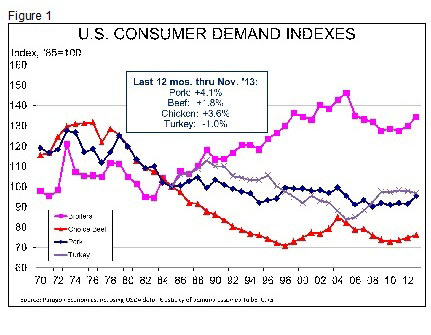

Figure 1 shows the now-familiar demand indexes for the four major species. Observations for years prior to 2013 reflect full year-on-year changes. The last observation for each series represents the 12-month period ending in November 2013. I do that because there is considerable seasonality in these indexes and using a 12-month running figure includes, by definition, an observation for every month. If we just included a year-to-date index for the last observation, it would be skewed due to it representing only a portion of a year’s seasonal pattern.

As can be seen, 2013 was a good year through November. If these numbers stand for the entire year, pork demand will enjoy its best year since 1998. (It’s hard to believe, but that financially disastrous year for pork producers was a good one for pork demand). Chicken will have its best year since 2002 and beef will have its best since 2004. Only turkey saw demand soften through November and that change was only 1 per cent.

Why the strength? I think that is a very, very good question. Recall first that demand is not quantity – it is the set of quantities that consumers will buy at alternative prices. Or, conversely, the set of prices that sellers can command for alternative quantities of product placed on the market. Both involve a whole set of price-quantity pairs. Changing the quantity of a product placed on the market does not change demand. It simply determines what the price will be. And conversely, changing the price does not change demand, it simply determines what quantity consumers will buy. These converse statements are applicable depending on what the decision variable is – quantity or price. The decision variable in meat and poultry markets is quantity as producers decide just how much product will be placed on the market at any given point in time.

So what determines the set of price-quantity pairs that constitute demand? Four things, three of which are significant. And how might they be impacting demand this year?

- Consumer incomes – People can buy only as much as their incomes will allow them to buy. Purchases of most goods (called “normal” goods) increase as income grows and decrease as it falls. Higher demand for meat can be the result of rising incomes. In fact, we know that income of consumers in China, for instance, is a driver of export demand for US pork. But the amount of money that US consumers have after inflation and after they pay their taxes - - ie. real disposable per capita income – has seen NO GROWTH since June 2008. Further, the average year-on-year growth rate for 2013 through November is 0.4 per cent. So higher demand is not being driven by robust incomes.

- Prices of substitute (ie. competitor) goods. But what if prices of all substitutes are higher? REAL retail beef prices grew by 4.6 per cent from January-November 2013. REAL pork prices increased 3.2 per cent. REAL chicken prices gained 2.7 per cent. REAL turkey prices fell by 0.2 per cent. I emphasize “REAL” in those statements to highlight that these are deflated prices, meaning that consumers have been willing to pay even more for beef, chicken and pork, than they have had to pay for all other goods (ie. the inflation rate). Turkey has about kept pace. Further, the indexes indicate that in the cases of those species, those price increases are LARGER than would have been caused by changes in the supplies of the products.

- Prices of complement goods. Theoretically, the demand for pork should be impacted by the price of barbecue sauce or applesauce or any other good that is considered to complement the use of pork. Ditto for beef and the price of baking potatoes, perhaps, or chicken and the price of dumpling mix (okay, I’m reaching on that one but you get my drift). Practically, though, these items are never statistically significant in demand research so I include them here as an academic courtesy to the profession and to prove to Drs. Leftwich, Lapan and others that I was listening at least part of the time.

- Tastes and preferences. The “economic speak” term that encompasses consumers’ individual and collective viewpoints about the desirability, or lack thereof, of a product. Flavor, versatility, religious restrictions, time of year, traditions and much more play into how consumers make their ultimate buying decisions. Tastes and preferences are the target of advertising and public relations campaigns – both for and against meat consumption.

So what is the sum of the factors? As pointed out, item 1 suggests demand should be constant. Consumers have no more money to spend so how could that drive demand higher? Item 2 offers evidence that consumer demand for meats has increased since the prices they will pay have risen faster than the prices of other goods and faster than production changes would suggest. Item 3 is, as described, a non-factor in reality. Which leaves item 4 – tastes and preferences – as the best reason to explain why item 2 (prices of substitute goods) indicates higher demand. It is difficult to believe that, amid all of the publicity about animal rights issues, undercover videos, the seemingly-nonstop caving (my judgment) of meat processors and sellers to the demands of activists, etc., etc., consumers could have stronger preferences for meat and poultry. The only things that support such a conclusion: The facts. I don’t fully understand it but the facts support it. Go figure.