China Hog Markets

CHINA - China: it is the pork powerhouse of the world with over 51 per cent of the world’s population of pigs raised within China, writes Ron Lane, Senior Consultant for Genesus China. 10 July 2014

10 July 2014

4 minute read

4 minute read

By:

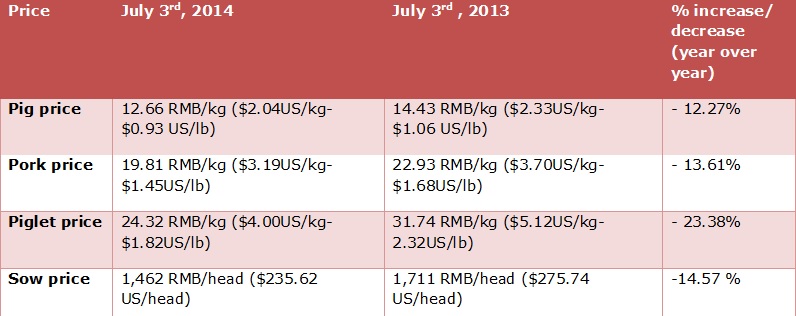

By: Looking at the size of the breakdown of the inventory for May, 2014, the information from MOA is indicating 428.09 million on farm inventory and a 46.40 million sow herd. The 428.09 million on farm inventory is down 0.1 per cent from last month and down 3.9 per cent from May, 2013. The sow herd is down 1.0 per cent from last month and is down 7.5 per cent from one year ago (May, 2013). Another 470,000 sows along with the 1.05 million sows from April were eliminated the past 2 months. The current sow inventory is the lowest level in 2 years. Hog production capacity has significantly been adjusted with the main cause being the loss of farm households. Despite the recent recovery of the market price for live pigs, several farm households are still in financial difficulty. MOA states that since the peak high of November 2013, the on farm inventory has dropped 8.6 per cent or about 36.9 million pigs…more than Canada’s total production for one year.

Factors such as disease, cold weather and/or home consumption (mainly backyard farms) for Spring Festival, have all affected the total on farm inventory. Recently, the low prices have been sending sows to market as small farmers are lowering the sow herd size or are totally quitting the business.

The large sell off of sows could cause a shortage of market pigs by the end of this year and thus a large increase in market pig and pork prices. This could have a large effect on the Consumer Price Index-something the national government does not like to see happen. Releasing national government frozen pork stock reserves will only soften the price increase over a short period of time. Low market pig numbers means higher prices and higher CPI.

Profit margins are now showing a further increase in losses from last month (still substantial losses). Recently, the farrow to finish farm was losing 163 RMB to 211 RMB/market pig ($ 26.27 USD to $34.00/market pig). On May 28th, the farrow to finish farm was losing 84 to 90 RMB/head ($13.54 to $14.50USD/market pig) and on April 11th, a farrow to finish operation was losing 357 RMB/head ($ 57.53 US/ market pig). Some analysts calculate that the loss for some newer, more financially leveraged farms is even higher. Compared to January 15th, it was reported that profits for a farrow to finish operation was 49.06 RMB/market pig ($ 7.87 USD/market pig).

The Consumer Price Index (CPI) continues to be quite interesting for the national government. Previously, when the pork prices were gaining, this rapid increase in pork, gained the attention of the national government as it greatly affects the CPI. The CPI is made up of about 30 per cent food found in the consumers’ basket. Pork is estimated to be about 1/3 of the food portion of the basket or in other words, about 10 per cent of CPI as a whole. CPI increased to 102.50 Index Points in May (2.5 per cent ) from 101.80 Index Points in April. This has been the highest CPI this year. The price of pork in China fell 7.2 per cent , contributing to a decline in the April CPI. As the prices increased in May, the CPI increased by 0.7 per cent . For now the pork prices are keeping the CPI lower, but a substantial increase, likely towards the end of this year, will cause national government concern. As a measure, when pig prices increase, CPI should increase.

What to watch for over the next few months:

- Last week (June 12th), the pig to grain ratio was 5.09:1. On May 28th, the pig to grain ratio was 5.43:1, up 2.27 per cent from the week before. On April 11th, the pig to grain ratio was 4.4:1; on February 20th, the pig to grain ratio was 5.49:1; and on January 15th, 2014, the pig to grain ratio was 6.18:1. This fell from 6.52:1 from the week before (January 8th). At the end of October, the pig to grain price ratio was 6.59:1.

- Currently, it is the 20th week with continuous pig to grain ratio that is below the breakeven point 6:1.

- Recently, the national average corn price was 2.54 RMB/kg.($0.41USD/kg-$0.19USD/lb.); wheat bran was 1.95 RMB/kg.($0.31USD/kg-$0.14USD/lb.) and soybean meal for retail to farmers was 4.10RMB/kg.($0.66USD/kg.-$0.30USD/lb). The average cost for feed was 3.28 RMB/kg ($0.53USD/kg-$0.24/lb)

- The WH Group, the largest pork producer in the world, had recently removed their IPO plans from the Hong Kong stock market. The Group, formerly known as Shuanghui and who bought Smithfield Foods last year, stopped the offer as not only because the Hong Kong stock market had dropped by 10 per cent , but also, there was a very weak demand for the shares as investors were staying away. The huge payments to company executives also helped to shut down the proposed IPO. Now US investment bank, Morgan Stanley is looking for solid investors for a deal priced at 20 per cent below the original offer from only a few months ago.

- Soybeans were China’s largest agricultural import during 2013. The Country brought in 38 Billion USD value of soybeans during 2013 with more than 1/2 from Brazil and close to 1/3 from the USA. Along the same vein, Bloomberg reports that China by 2021 will become the world’s largest corn importer. This year, China is expected to import about 2 per cent of its total consumption. This will increase each year so that by 2024, it could import 7.2 per cent of its needs.

.jpg)