CME: USDA Hogs and Pigs Estimates

US - So much for the bearishness of USDA’s September Hogs and Pigs Report. After opening the session with most contracts trading $2.00 or more lower, the market appeared to shrug off the report with closing prices mixed relative to last Friday, writes Steve Meyer and Len Steiner. 1 October 2014

1 October 2014

2 minute read

2 minute read

By:

By: Nearby (through February) contracts ended higher for the day’s pit trading session while the deferred contracts were down 20 to 50 points. Overnight trading has every contract through August 2015 higher with July leading the way at +75 points. So what happened to the expected bearishness of this report?

Especially when every key number was larger than what analysts, on average, expected. First, it appears that analysts, on average, may not represent the true sentiment of the market. That is always a possibility in these matters and it is more so with the livestock contracts because the pre report surveys involve a pretty small sample.

Last week’s Urner Barry survey had nine respondents. Bloomberg’s had twelve. Most grain production surveys have upwards of 20 data points. We’re not being critical and we appreciate the analysts that provide estimates.

The fact remains that the sample is small. Second, the futures market has followed a pattern of discounting the deferred hog contracts for some time. We think that is due to the huge level of uncertainty surrounding PEDv and the fact that if a solution is found, it will be adopted and have an impact quickly.

That caution has apparently gotten larger as another vaccine has been made available and the number of case accessions have declined. That latter of those is primarily due to warmer weather but producers are resourceful and will very likely be able to manage the disease better this year than last.

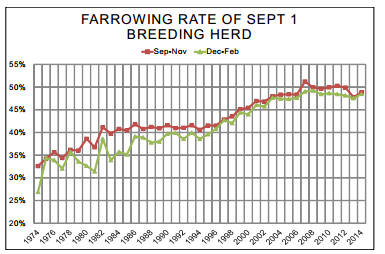

Bottom line: Futures were already reflecting much larger supplies for 2015 before this report was released. And then there are a couple of question marks. On first glance, we thought the farrowing intentions for September-November and December-February looked very high relative to the breeding herd.

We know that producers have bred heavily given profit potentials and concern over sporadic PEDv cases that will reduce the numbers of pigs produced even if full?blown outbreaks can be avoided. But those numbers still looked ambitious – until we compared them to history. Turns out our concerns were unfounded as the implied farrowing rates for both quarters are still below their pre 2013 levels. Our other question mark is more serious, though.

USDA quite correctly revised its December-February pig crop downward by 3.6 per cent to reflect the amount by which slaughter this summer has fallen short of the level implied by its original estimate. Good for USDA. The original estimate was obviously off. But USDA apparently ascribed the entire error to a miss estimation of farrowings as it changed that estimate for December-February by the same percentage — thus leaving the number of pigs SAVED per litter the same.

USDA adjusted both the pig crop and farrowings in the same manner for June-August and September-November of 2013. Does this make sense in the face of a disease that does not generally kill sows or cause many abortions but kills pigs AFTER they are born.

Changing the pig crop is absolutely correct but it seems to us that the number that should change to accomplish that is PIGS SAVED PER LITTER. And that number is VERY IMPORTANT this year since we will now all be trying to figure out how pigs saved per litter has changed from last year’s level in order to estimate just how many pigs will come from those higher farrowings this fall and winter.