November US Export Data Good News and Bad News

US - The November US export data was one of those bad news-good news things, writes Steve Meyer for the National Hog Farmer. 13 January 2015

13 January 2015

4 minute read

4 minute read

By:

By: First the bad news: Exports were down again on both a month-over-month and year-over-year basis. Total U.S. pork exports of 364 million pounds, carcass weight equivalent, were 4.4 per cent lower than in October and 19.8 per cent lower than one year ago. November exports leave the year-to-date figure at 4.464 billion pounds, carcass equivalent, down 1.7 per cent from one year earlier.

In spite of being lower than last year since June, November marks the first month this year in which the YTD figure has been lower. Do not expect that to improve when December data are released in early February.

There was no single problem in November as virtually all U.S. export markets took less product than they did one year ago. Some of the reductions were dramatic: Russia, of course, was 100 per cent lower, China was down 74 per cent , Japan was down 22 per cent and Canada was down 10.7 per cent . Even Mexico, which had taken more U.S. pork than one year earlier in every month since March 2013 took 11 per cent less U.S. pork in November than it did one year ago. Only South Korea (+23 per cent ) and the Caribbean (+5.5 per cent ) took more pork this November than they did last year.

We will have only two growth markets for 2014 when the year is wrapped up. Mexico is our largest market now and is up nearly 13 per cent through November. Even a bad December will leave them positive and still the largest (Mexico has about a 100 million pound lead on Japan through November). The other growth market is Korea, where US exports are up 41 per cent through November. That growth rate is from quite disappointing export levels last year but is encouraging nonetheless.

Why the slowness in exports? Being an economist, my first answer is price! Record high US prices and an appreciating dollar (see Figure 1) have made US product more expensive for virtually every foreign customer. Add in a few boat loads of what was once European Union (EU) exports to Russia that have had to find a home since last spring and you get a “challenging export environment”. That EU product amounted to 40,000 metric tons per month early on. That figure could be less now but it is still substantial.

The dollar is nowhere near record highs but did close last week (Figure 1 is a weekly chart for the nearby Dollar Index contract) at its highest level since late-2003.

What is in store next year? The US Department of Agriculture’s World Agricultural Outlook Board raised its forecast for next year by 255 million pounds in today’s World Supply and Demand Estimates. That number is 3.5 per cent higher than this year. It is driven by a production forecast that is 4.6 per cent larger and the fact that this higher output will indeed cause prices to be lower. The growth appears a bit aggressive to me but U.S. export performance has exceed my expectations regularly over the years.

And the good news? The lower exports meant more product in the United States. “That’s bad news,” you say. Well it could be, but in this case the increase in availability did not push prices lower by much. The fact that more product was consumed versus one year ago and the price decline was small implies that pork demand remained strong. In fact, it was great once again in November.

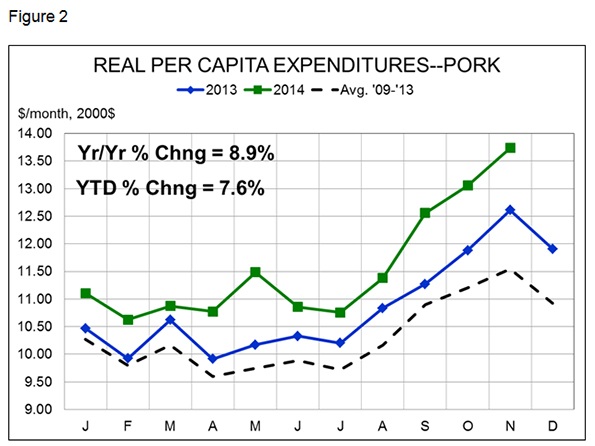

Figure 2 shows real per capita expenditures (RPCE) for pork for each month this year. November’s $13.74 (in year-2000 dollars) was the highest single monthly figure since December 1991. It was 8.9 per cent higher than last year and brings this year’s YTD RPCE to $112.99 (also in year-2000 dollars), a figure 7.6 per cent larger than last year and 12.6 per cent larger than the average for January to November of the past five years.

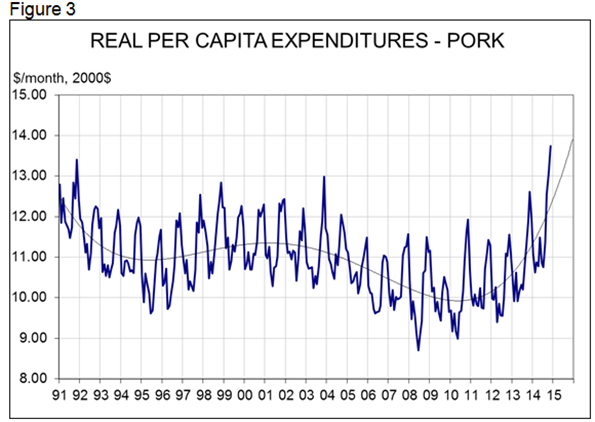

The growth of pork RPCE since 2010 has been impressive (see Figure 3) and the growth in 2013 and 2014 has been almost astonishing. High beef prices and higher-than-expected chicken prices have been a big help but consumer income levels have been pretty much neutral until, perhaps, the past three months. I still think the big driver is consumer preferences for protein and reduced negative connotations for animal fats. The coming year will see strong beef prices continue but increased competition from chicken. The economy seems to be picking up so consumer incomes may grow and lower gasoline prices will leave US buyers with more discretionary funds even if they don’t.

We apologize for the lack of Canadian data. Stats Canada has not published weekly data since Dec. 27.

Finally, congratulations and welcome to Chris Hodges as the new chief executive officer at the National Pork Board. Hodges is a long-time friend who has a wealth of knowledge about the industry, working for many years for Farmland Foods and, since its merger with Smithfield, for Smithfield-Farmland. The challenges are big but he is a worthy choice to lead the NPB and the Checkoff.