CME: Latest RPCE Figures Barely Positive for Pork

US - Last week’s April trade data provided us with the last piece of information we needed to compute April per capita consumption figures and thus real per capita expenditures (RPCE) for the month and the story was still positive - but barely so for pork, write Steve Meyer and Len Steiner. 11 June 2015

11 June 2015

2 minute read

2 minute read

By:

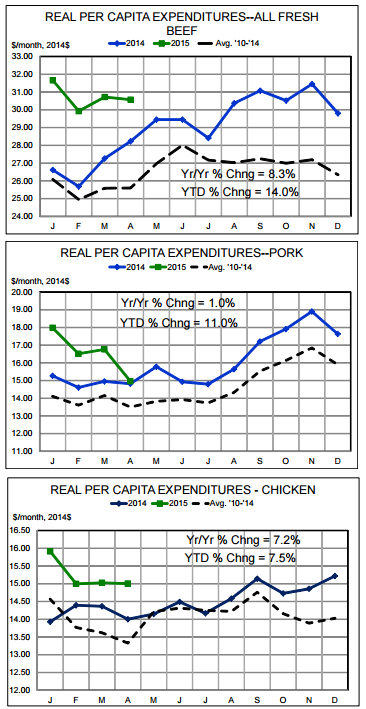

By: The charts below show monthly RPCE data for 2014, 2015 to-date and monthly averages for 2010-2014.

We discussed last week that a number of factors are still pointing to strong demand, especially in the foodservice area. The results from April point to continued strong demand growth for beef and chicken and a year-on-year squeaker for pork, but that final result may be a relic of some unusual data. More later on that topic. Let’s consider the highlights.

Beef demand continues to grow and a strong 8.3 per cent realtive to one year ago in April. The month’s RPCE of $30.57 in 2014 dollars was down slightly from March. It brought the year-to-date total RPCE for beef to $122.86, 14 per cent higher than on year ago and 20.2 per cent higher than the average YTD figure for April for 2011 through 2014. April is the first month since July that the year-on-year increase for beef RPCE has been less than 10 per cent !

Note that we use the All-Fresh retail price from USDA in our beef calculations since it represents more beef (Choice, Select and store grade) products in the retail case than would just the Choice price. We computer both and the year-on-year comparison are almost identical though the actual dollar values of RPCE using the All?Fresh price are, as one would expect, lower than their Choice grade counterparts. As has been the case for over two years, the retail beef prices (+10.4 per cent , yr/yr) was the big driver of the April RPCE gain. Per capita consumption was down 2.2 per cent from one year ago.

Pork demand, which had been flying high, moved sharply lower in April - or did it? The computations show that RPCE fell from March’s $16.76 (in 2014 dollars) to $14.96 in April, a drop of over 10 per cent .

The April value is still 1 per cent higher than one year ago an d leaves year-to-date total RPCE at $66.21, 11 per cent higher than last year and 19.6 per cent higher than the 5-year average. We say “or did it” because the pork data were complicated in April by a resurgence of exports and growth of freezer inventories which both pushed per capita supply/disappearance/consumption down from its lofty March levels. April per capita consumption was still 5.6 per cent higher than one year ago.

Pork prices dropped below year-ago levels for the first time since February 2013 but the year-on-year price decline was still not enough to offset the increase in per capita consumption. The April surge in exports was likely enhanced by the end of the West Coast port slowdown and it is very likely that USDA’s average retail pork price will stabilize this summer as wholesale values have risen once more.

Chicken RPCE had another “steady as she goes” month with RPCE remaining at $15.00 in April. That is virtually even with the prior two months though it is farther ahead of last year’s figures (by 7.5 per cent ) since RPCE declined in April 2014.

Nominal retail chicken prices rose 3.5 per cent, year-on-year, while per capita production/disappearance/consumption went up 3.3 per cent during the month. Higher real (deflated) prices and higher per capita consumption can mean only one thing: Higher demand.

We expect these RPCE’s to remain above 2014 levels for the foreseeable future. Meat and poultry protein is much more accepted.