CME: US Hog Inventories, Breeding Herd Up

US - USDA will soon publish the results of its quarterly survey of hog breeding and finishing operations, write Steve Meyer and Len Steiner. 25 June 2015

25 June 2015

4 minute read

4 minute read

By:

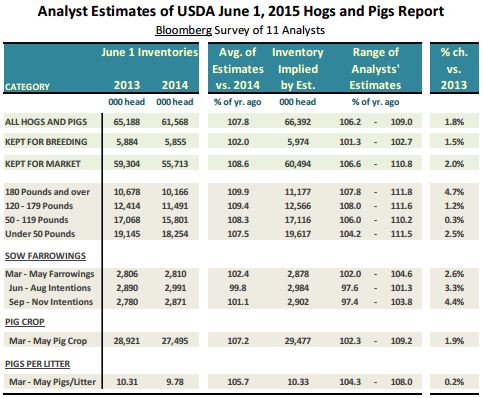

By: Ahead of the report Bloomberg surveyed 11 analysts and a summary of their estimates is presented in the table to the right.

The numbers are presented as per cent of year ago levels but we thought it also makes sense to show how the numbers compare to 2013 - when PEDV did not dramatically skew the numbers.

Hog Inventories: On average analysts expect the total inventory of hogs and pigs as of June 1 to be 7.8 per cent higher than a year ago but 1.8 per cent higher than in 2013.

Inventory of market hogs is expected to be 8.6 per cent higher than in 2014 but it is only 2 per cent higher than in 2013.

Hog slaughter numbers in the last few weeks have been running a bit higher than what was implied in the March report.

Analysts expect inventories of hogs over 180 pounds to be 9.9 per cent higher than last year, which is a bit low considering that in the first three weeks of June (we are estimating current week) hog slaughter as averaged 11.3 per cent above year ago levels.

Forecasts are for hog slaughter numbers to remain significantly higher compared to last year in Jul - Nov but pay attention to the comparison to 2013.

Inventories of hogs 120-179 pounds (normally would come to market mid Jul through mid to late Aug) are currently forecast to be 1.2 per cent higher than what they were in 2013.

August hog futures currently are priced at around 72 cents compared to around 94 cents in August 2013. Hogs are certainly heavier, which should bolster supplies compared to two years ago but still, futures at this point appear to be pricing a larger supply of hogs coming to market than the average of analysts’ estimates.

Inventories of hogs between 50-119 pounds are expected to be 8.3 per cent higher than a year ago but just 0.3 per cent higher than what they were in 2013. These are hogs that should roughly come to market from late August to mid October.

Compared to last year, numbers certainly are plentiful but the analyst estimates reflect more of a return to trend rather than dramatic jump in supplies.

It is always possible that estimates from analysts could be understating the supply picture and we can make an argument that some numbers indeed should be a bit higher than the average levels.

Analysts, for instance, expect the pig crop during Mar-May to show a 7.2 per cent increase compared to a year ago and 1.9 per cent higher than in 2013.

This pig crop reflects farrowings and pigs saved per litter during this period. Farrowings are projected to be up 2.4 per cent, slightly higher than what was expected before.

The ratio of farrowings to the breeding herd for Mar-May is implies a lower level than what we have seen in years prior to PEDv. Could we see a surprise in this number?

The range of analyst estimates is from 2 per cent to 4.6 per cent, indicative of the possibility of larger numbers, which in turn would imply higher market hog inventories.

We think the number of pigs saved per litter at 10.33 is in line with the normal increase for the time of year and reflects a normalisation in hog production after the devastating losses of 2014.

Breeding herd: The average of analyst estimates implies a breeding herd as of June 1 of 5.974 million head, 2 per cent higher than a year ago.

There is a very wide range of estimates, which strikes us as a bit odd considering we do have a fairly good idea about the number of breeding animals that went to slaughter in the past quarter as well as those that were imported from Canada.

What is always a big unknown is the number of gilts retained but one needs to make some very dramatic forecasts about gilt retention in order to get a breeding herd that is up just 1.3 per cent from last year.

Our forecast is for the breeding herd to be up 2.3 per cent. This implies a modest slowdown in gilt retention as well as sow slaughter in the quarter up 3.5 per cent (this is based on weekly numbers).

Based on analyst estimates, the breeding herd is up 1.5 per cent from 2013 levels but the number of pigs saved per litter (and hence the pig crop) is expected to remain large for the remainder of the year.

The big wild card this coming fall and winter remains PEDv as some of the sows that are coming into production will not enjoy the immunity of the previous stock.

At this point futures are pricing ongoing expansion but risk premiums for next summer may start to creep back in if the disease starts to show up later this year.