CME: Hog Price Decline to Impact Producer Returns

US - The recent declines in hog prices will reverberate throughout the marketing chain, but the most noticeable near-term impact will likely be on hog producer returns, write Steve Meyer and Len Steiner. 30 November 2015

30 November 2015

3 minute read

3 minute read

By:

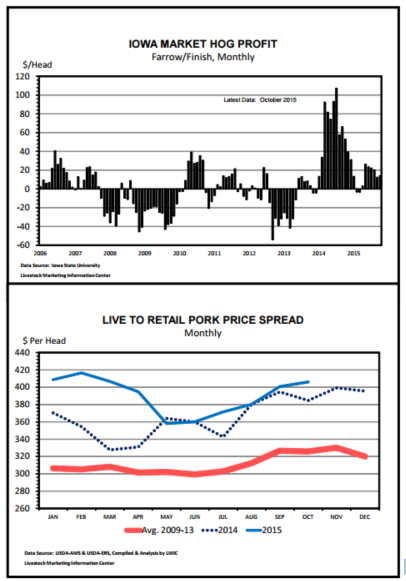

By: In October, compared to a year ago, hog producer returns were down as were estimated margins (price spreads) for the packers. In contrast, calculated margins at the retail level were above 2014’s.

Through the month of October, farrow-to-finish hog producers turned profits for six consecutive months in recent months as indicated by Iowa State University (ISU) estimates. Note that those estimates include all economic costs, not just cash expenses. Total feed costs for animals sold in October were the lowest in years.

For slaughter hogs the breakeven sale price (October price required to cover costs for animal production) was estimated at $61.70 per cwt. versus an Iowa sale price of $69.31. For October, ISU calculated profit at $9.72 per head without accounting for the value of manure produced and after including that value, a profit of $13.98.

From May through October ISU estimated returns mostly in the $12.00 to $26.00 per head range, rather large by historical standards, but well below the record large profits posted in 2014. Lower slaughter hog prices in November suggest red ink has returned for farrow-to-finish operations.

December and at least January look to be more of the same. Still, typical producers will be able to cover all their variable production costs (feed, etc.) and some of their overhead costs, so financial hardship should not occur. Breeding stock liquidations are not likely, however herd growth plans are likely to be tempered.

Turning our attention to margins beyond the farm level in the hog/pork industry, wholesale and especially retail prices adjust more slowly than do those at the farm-level.

During October, slaughter hog prices (weekly average national net carcass) dropped by $1.89 per cwt. or 3 per cent. In that same timeframe the cutout (wholesale carcass equivalent value per USDA’s Agricultural Marketing Service Market News reports) also slipped 3 per cent. So far in November, live animal prices have declined much more than wholesale – weekly average slaughter hogs fell 19 per cent while the pork cutout dropped by 11 per cent.

Estimated packer margins calculate the difference between live animal price and the wholesale meat value plus byproducts (non-meat items); referred to as the live to cutout price spread. Note, that this margin or spread does not include all costs of production, is excludes packing plant labor, transportation, facilities costs, etc.

In October, the live to cutout spread was higher on a per head basis than any prior month in 2015, but was 9 per cent below a year earlier (down just over $4.80 per head live animal basis). Of course, some of that decline is due to much lower byproduct (non-meat) values. Packers in recent months have been profitable, and November will be improved from both October’s level and a year ago, due largely to lower live hog costs.

A Retail margin is calculated similar to that for a typical packer; it’s the difference between the cutout value and the USDA Economic Research Service’s calculated retail price, which is estimated from data collected to calculate Consumer Price Indexes and uses several assumptions. So, caution is required when looking at the cutout to retail price spread, the focus should be on year-over-year change rather than absolute levels or short-term comparisons. As with the packer margin, many retailer costs are not included. In October, the cutout to retail price spread was 8 per cent above a year ago.

Combining the packer and retail price spreads together gives a live to retail margin, which is depicted in the accompanying graphic on a per head basis. That is sometimes referred to as the total marketing margin, for hogs/pork in October it was about 6 per cent above a year earlier.