CME: Hog Slaughter Expected to be Near Annual Highs

US - Following the Thanksgiving holiday, Steve Meyer and Len Steiner offer their thoughts on the supply considerations for the three main meat proteins. 1 December 2015

1 December 2015

2 minute read

2 minute read

By:

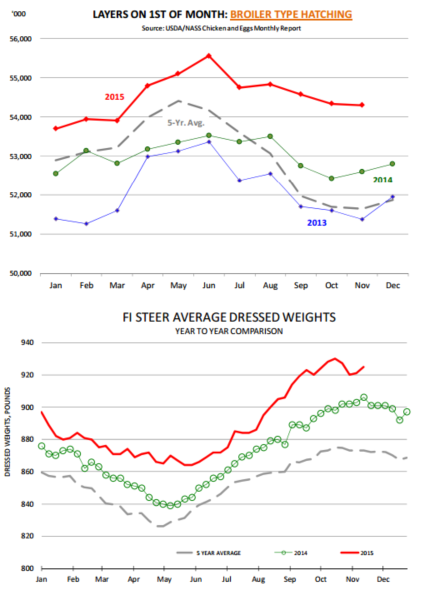

By: Chickens: There have been no cases of bird flu this fall despite earlier fears that a return of the disease could cause widespread losses and significant chicken price inflation. At this point the broiler industry is coping with burdensome stocks in cold storage, weaker than expected export demand (currency, bird flu bans) and seasonally lower demand for chicken breasts. There has been some effort on the part of producers to limit the number of eggs sets and chick placements.

In the last four reported weeks, egg sets are down 0.9 per cent from a year ago while chick placements are down 1 per cent. However, bird weights continue to run notably higher than a year ago and this has offset any reductions implemented. There is a limit as to how quickly the broiler industry can cut back.

Strong margins in 2014 and early 2015 encouraged expansion of the hatching flock and the expansion of the production base persists. USDA reported last week that the number of broiler type hatching birds as of November 1 was 54.299 million, lower than the previous month but still about 3.2 per cent higher than a year ago.

Seasonally the number of broiler type layers declines in the fall but so far the seasonal decline has been much smaller than normal. The size of the layer flock has not returned to 2000-07 average but it does not have to be. The increase in bird weights implies that a smaller layer flock is needed to generate the same amount of production.

The layer flock in 2007 average 57 million and broiler meat production was 35.8 billion pounds (RTC weight). In 2015, broiler production is expected to be almost 40 billion pounds while the hatching flock will likely average around 54.4 million head. The outlook is for continued expansion of chicken production in 2016 both in terms of the number of broilers coming to market as well as further (albeit smaller)

Beef: Front end cattle supplies remain larger than a year ago although the overall cattle supply availability is small by historical standards. There was some hope in October that feedlots were finally ge?ng their arms around the backlog of cattle that developed over the summer. The decline in steer carcass weights was seen as evidence that feedlots were becoming more current. But, steer weights have been climbing again and there are growing concerns that sticky beef prices at retail (retail prices remain near record highs), weak exports and lower byproduct values will limit packer demand for cattle and continue to back up cattle in feedlots.

Recent weather storms have provided some support for futures. There is also some hope that more ground beef features in January will help clean up the backlog of grinding beef and underpin end cut values in early 2016. At this point that remains a hope and wholesale prices are much lower than earlier expected.

Pork: Hog slaughter is expected to be near annual highs into early December following a holiday shortened week. The September Hogs and Pigs report implies that hog slaughter in Q1 will remain near the 2.3 million mark.

Hog carcass weights also are expected to be at or even above the record levels of 2015, further bolstering pork production. This could limit the upside the hog market, at least in the short term.

Exports will be key for pork in the first half of 2016. Without robust export demand, we will see higher per capita supply availability in the domestic markets and lower prices may be needed to absorb it.