CME: Livestock, Poultry Producers Benefited from Benign Feed Markets

US - Livestock and poultry producers have benefited from benign feed ingredient markets so far this year, write Steve Meyer and Len Steiner. 17 March 2016

17 March 2016

2 minute read

2 minute read

By:

By: Corn prices, basis the nearby futures contract, have traded in a 20 cent per bushel range since the start of the year, down 10 per cent from a year earlier and down 20 per cent from two years ago.

Last week, the USDA in its World Agriculture Supply and Demand Estimates (WASDE), made no significant changes to its corn market forecast, except to narrow the price range for expected prices this crop year to $3.40-$3.80, shrinking from a 50 cent range in February. Since the start of the crop year last September, corn prices at the farm have averaged $3.65.

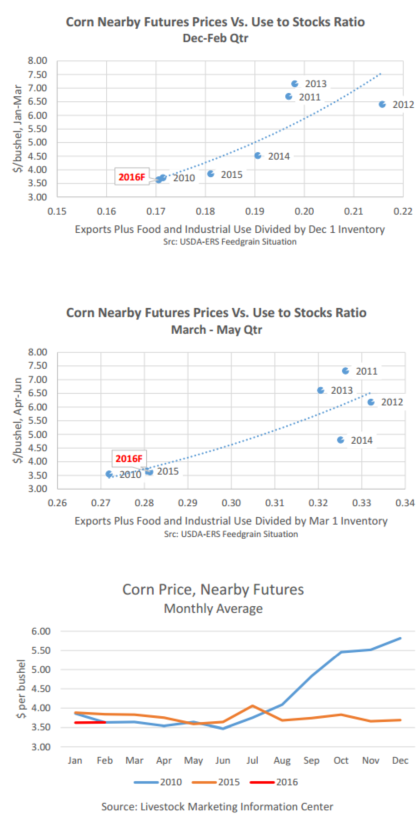

Corn prices on the nearby futures contract have averaged close to $3.60 since the start of 2016. This price is consistent with price behavior since 2010, relative to inventories at the start of the winter quarter (December 1, 2015) and corn volumes moving to export destinations and domestic usage for food or industrial (e.g. ethanol).

Combined usage from these sectors amounts to 17 per cent of inventories on hand at the beginning of the quarter. Prices and usage have been similar to the same quarter in 2010. According to the USDA-WASDE forecast, food and industrial use this crop year is expected to be up half a percent from the prior year. Usage was up 1 per cent during the September-November quarter and winter quarter usage is expected to be close to unchanged from a year earlier.

The USDA-WASDE forecast shows a 10 per cent export decline this year, with exports during the first six months of the crop year running down more than 20 per cent. This would imply moderating declines in exports during the last half of the crop year.

The top scatter-plot shows that corn markets get exciting when the ratio of usage to stocks during the winter quarter gets close to, or exceeds 20 per cent.

The difference between this year’s 17 per cent and prior year’s 20 per cent is huge. Similarly, March-May usage to stocks ratios above 32 per cent are more interesting than ratios below 30 per cent. Based on expected inventories on March 1 and projected MarchMay usage consistent with USDA-WASDE forecasts, the March-May usage to stocks ratio calculates to be 28 per cent. This should translate into an average nearby corn futures price of $3.50 for the April-June quarter.

Again, these conditions run close to 2010, as well as the 2015 corn market. The graph at the right contrasts corn price behavior in 2010 and 2015 for the entire year with this year’s prices as a point of reference. At least for the next 2-3 months, livestock and poultry producers should find feed cost risk easy to manage.