CME: Analysts Expect Pig Breeding Herd at Over 6 million

US - Following yesterday’s discussion of the spike in hog slaughter, it seems appropriate to review what analysts are thinking as USDA gets ready to release the results of its quarterly ‘Hogs and Pigs’ survey, write Steve Meyer and Len Steiner. 29 September 2016

29 September 2016

2 minute read

2 minute read

By:

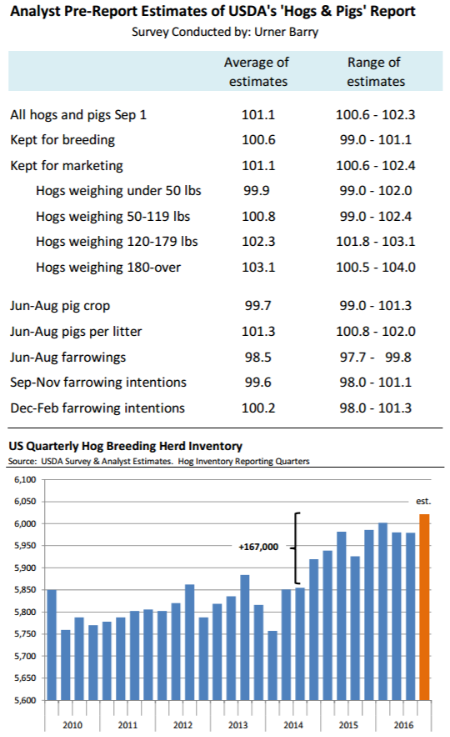

By: Front end supplies: Hog futures have sold off aggressively in recent weeks and they were down again yesterday, with December futures now trading at 46 cents, down about $12/cwt (‐21 per cent) compared to a month ago. The selloff is tied directly to the spike in hog slaughter numbers, as producers look to get current in their marketings but it also reflects worries that supplies on the ground are bigger than the June survey suggested.

The average of analyst estimates does not depart much from the June report. Hogs weighing over 180 pounds are pegged at +3.1 per cent higher than a year ago. So far in September, however, slaughter is running at +5 per cent, meaning we are pulling hogs forward. But if that’s the case, producer weights this week should start to bend lower. Inventories of the next two categories will be critical in terms of challenging processing capacity.

Based on the analyst estimates we will get close to the ceiling but not bump up against it too much. They certainly do not warrant hog prices in the low 40s. Indeed, if analysts are correct, hog slaughter in November and early December may be only marginally higher than what we are seeing today.

Needless to say those two weight categories will be watched closely given worries about processing capacity availability later this year.

Breeding herd: This has always been a critical number and this year is no different. Low feed costs and excellent margins in the last couple of years have fueled hog industry expansion. Analysts on average expect the breeding herd inventory as of September 1 to be 0.6 per cent larger than a year ago. If correct, this would peg the inventory at over 6 million head, +167,000 head more than what we had at the end of 2014.

A larger breeding herd was initially thought to be good insurance against disease losses. However, disease pressures have been minimal in the last two years. The combination of more breeding animals and more pigs per litter has bolstered quarterly pig crops and fueled the demand for more processing capacity.

A number of new plants are in various stages of completion. It will be interesting to see, however, what kind of increase we see in breeding animals. There is anecdotal evidence that more sows are on the ground and sow slaughter rates for the past Jun‐Aug quarter are lower than the previous year. So while the forward profit outlook has changed dramatically in the last few weeks, the question is what kind of supply have we inherited to this point.

Farrowings and pigs per litter: Analysts expect June‐Aug farrowings to be down 1.5 per cent while pigs per litter are forecast at +1.3 per cent. Based on current trends, it seems to us both these numbers are on the low end. We would have expected to see farrowings under 1 per cent, probably down about 0.6 to 0.7 per cent and pigs per litter at +1.5 to +1.6 per cent. For now, it appears that the analysts are quite conservative in their estimates. Hog futures appear to be trading a much more bearish outlook for hog supplies into next February than what analysts are presenting in their estimates. Sep‐Nov farrowing intentions are pegged 0.4 per cent under last year, which does not match well with the expanding breeding herd.