CME: Hog Slaughter Numbers Truly Shocking

US - Hog slaughter numbers last week were truly shocking and the fear is that hog supplies on the ground are larger than what packers are able to process during a regular work week, write Steve Meyer and Len Steiner. 28 September 2016

28 September 2016

3 minute read

3 minute read

By:

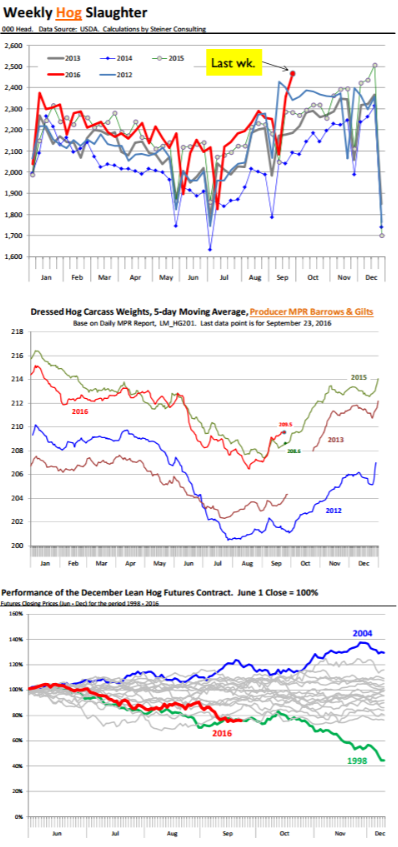

By: The last time “normal” processing capacity was exceeded was in the fall of 1998, when hog prices briefly dropped in the single digits. At 2.466 million head, weekly hog slaughter last week was 8 per cent larger than a year ago and far bigger than one would expect based on the June ‘Hogs and Pigs’ report.

That report pegged the pig crop for Mar ‐ May (which corresponds to slaughter in Sep ‐ Nov) at +2.5 per cent higher than the previous year.

Last week’s numbers represented the largest weekly slaughter for this time of year and the third largest ever. Seasonally hog slaughter continues to move up in October, November and early December and the spike in slaughter last week has some worrying we could surpass 2.5 million

head/week. At these levels, marketing hogs becomes particularly challenging.

Dr Steve Meyer has been diligently tracking packing capacity for a long time and in 2015 he pegged weekly capacity (based on a 5.4 day week) at 2.442 million head. There were a couple of smaller operations that were supposed to come online this fall, which would add about 35,000 head per week to that total but overall weekly capacity still is under 2.5 million head.

Looking for a silver lining. At this point futures have not priced the potential for a complete collapse in hog price similar to what we saw in 1998. But as the bottom chart shows, December hog futures so far have tracked almost exactly the trajectory of the December futures contract in 1998. The other gray lines represent other December contracts between 1998 and today.

There have been other years which have seen a similar decline in futures values between June and September but only in 1998 did we see December hog futures post a 60 per cent decline from June levels.

The hope among market participants is that producers recognize the precarious situation with regard to processing capacity and will work hard to pull hogs forward. Indeed some may view the most recent spike in slaughter as evidence of just that. The problem with this, however, is that if producers do pull hogs forward then we should see a response in terms of the weight of hogs coming to market.

So far, there has been no sign that weights are coming down or at least moving sideways. Consider what happened in 2012. Back then, producers pulled hogs forward, in part because of the spike in feed costs, and the average weight of barrows and gilts sold by producers declined some 1.5 per cent between mid September and early October. The increase in slaughter in mid September 2012 is reminiscent of what happened last week.

So far weights have moved up even as hog slaughter has far outpaced the pig crop estimates. It will be critical to observe the performance of hog weights this coming week. Another hope among market participants is that producers and packers today work more closely and are better integrated than they were 18 years ago. The hope is that all involved will do a better job of managing the flow from farm to the packing house.

Pork demand for now has been ok even as exports could be better and ham inventories are large. Demand may be challenged going into Thanksgiving and year end holidays given ample beef and chicken supplies.

But for now, the real worry in the market is the ability of producers to market hogs in a timely manner and avoid the 1998 debacle. Needeless to say, there is be plenty of anticipation ahead of USDA’s September ‘Hogs and Pigs’ report (Friday, 2PM CST).