US Pork Cutout Outperforms Last Year's Levels

US - The pork cutout has outperformed year ago levels despite notably more pork available on a daily basis in the marketplace, writes the Steiner Consulting Group. 6 December 2016

6 December 2016

3 minute read

3 minute read

By:

By: Hog slaughter in the last four weeks averaged 4.4 per cent above year ago levels and even when adjusting for a 1 per cent decline in weights total pork production has averaged 3.3 per cent above last year. This week we expect slaughter to be up about 2 per cent from last year while production should be around 1 per cent from a year ago. Lower prices for pork earlier in the fall appear to have “bought” some preƩy good demand going into the holiday season.

Robust export volumes also have helped clean up the market, with particularly strong exports to Mexico despite a steady erosion in the value of the Peso.

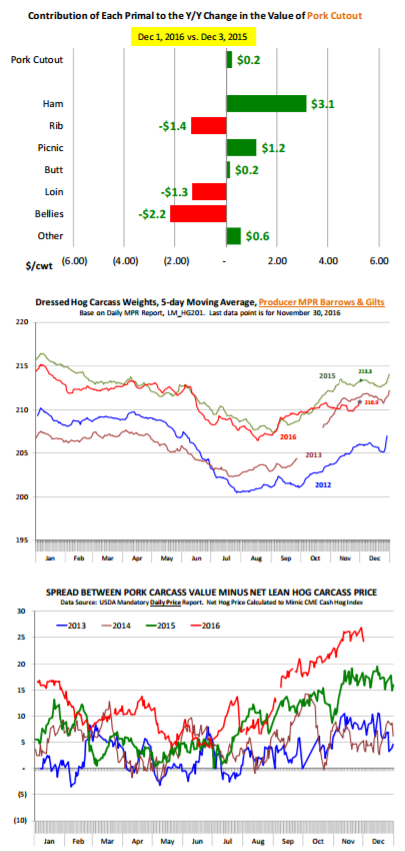

The chart below shows how each primal has contributed to the overall improvement of the cutout vs. year ago. The pork cutout last night was quoted by USDA at $74.31/cwt, about $0.2/cwt (+0.3 per cent) higher than a year ago. A number of items are down from last year. The value of the belly primal at $98.1 is down $13.74/cwt (‐12.3 per cent) from last year, which deducts about $2.2/cwt from the overall cutout. The loin primal last night was $66.44/cwt, down $5/cwt (‐7 per cent) from last year, removing another $1.3/cwt from the cutout. However, the decline in the value of bellies and loins has been more than offset from higher ham values.

The ham primal last night was quoted at $77.74/cwt, $12.77 (+20 per cent) higher than a year ago. Part of the reason for the robust ham value is certainly due to stronger demand as pork supplies continue to outpace 2015. But a change in how USDA calculates the primal value also appears to have contributed to the big gains in the ham primal. Consider that the price of #23‐27 hams yesterday was $72.87/cwt, $5.23/cwt (+7.7 per cent) higher than a year ago. Prior to the change, the primal would for the most part reflect the value of the #23‐27 hams. However, as more boneless product has been added to the mix, this has bolstered the value of the primal, which is now about 20 per cent above year ago levels. Boneless hams have been trading much higher this year as packers struggle to find enough labor to both run maximum slaughter and also man boning lines.

Further processors also have been struggling to keep up with the amount of hams that are being generated. At this point boneless ham muscles (insides/outsides) are trading at a 2.3 multiple relative to bone‐in large hams compared to a 1.5 multiple last year. In the short term, the challenge for the pork cutout is that hams will lose value once Christmas orders for fresh product have been filled. The question is by how much. And with large slaughter volumes, it is hard to see bellies and loins performing much better than last year.

For the moment, cash hog values have improved and for good reason. Producers were quite aggressive in marketing hogs early in October and November and by doing so they appear to have avoided a wreck in December. But this does not mean that hog supplies will not stay heavy for a few more weeks. The focus of the market in the last two months has been almost unwaveringly on supply risks, first pricing sharp discounts and then taking them back as the crash was avoided.

After the first of the year, the focus will turn to demand, both domestic and export. Last year resurgent China demand helped hog prices rebound in February and then again in April while Mexico was the big story this fall. At this point market is still looking for a Q1 theme.