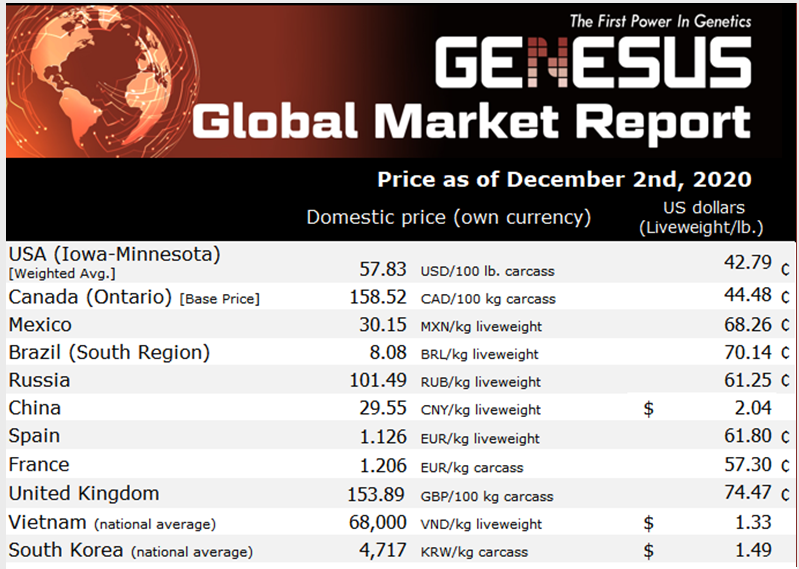

Genesus Global Market Report Canada, December 2020

I was encouraged recently to attend an open house for our newest multiplier in Ontario. There was a good turnout with very high percentage of younger producers. I guess I am of the age to be seeing generational turnover, but it is encouraging to see so many new entrants into the business. 7 December 2020

7 December 2020

4 minute read

4 minute read

By:

By:

This is a rare phenomenon that I don’t believe is happening in too many other places. These are all independent producers, mostly carrying on from a previous generation of independent producers. Ontario remains perhaps the last bastion of independent producers which are becoming an increasingly endangered species in most jurisdictions. My review below of my last five commentaries of the past year suggests why. To the point that you would wonder why anyone would come into this business.

However, I’ve seen encouragement come from the previous generation in various forms but runs something like this. “Dirt farming will make you a living but just that. Hogs are what bought the next farm, built barns and houses, educated kids. You need to walk the corn off the farm”.

This model of land to corn to hogs to manure and back around has proved a remarkably sustainable model providing ballast through hard times. Again, as demonstrated below it has been sorely tested in the past couple years.

The Progressive Pork Producers producer-owned packing plant Conestoga Meats has further strengthened that hand allowing approximately a third of the industry a better share of packer margins. That has amounted to at least fifty plus dollars over counterparts in the past year and more. The remaining two-thirds have challenges. Packing capacity and vitality is a serious governor to growth for this industry.

Olymel (a Quebec packer) seem to have ongoing reasons why they can’t get their Ontario contracted slaughtered, from strikes to cooler issues to Covid to… Also, their preferred option seems to be integration like so much of their business in Quebec and Western Canada.

I have discussed in earlier commentaries the fork in the road for Ontario producers as to whether to integrate up or down. Integration up certainly has its challenges as demonstrated by the twenty-plus year climb of Progressive Pork Producers but today seems quite insightful. The question becomes can it continue to grow or perhaps be duplicated? The integration down allows you to survive but at what level above “bread & water”?

The middle path practiced by Sofina (the other major packer in Ontario) is the more traditional packer doing what he does best, with producer doing the same. Then receiving their share of the pie as to the strength of their hand. This is the oldest method but is it sustainable going forward?

Below is a review of the profitability minefield producers have had to find a path through. Seeing some of the next wave of up-and-coming producers I am more than encouraged that their resilience, inventiveness and received wisdom of their forebearers will stand them in good stead.

From Canada Market Report_October 5, 2020

In my last commentary, I questioned whether the industry was broken perhaps permanently. Now, eight weeks later we have this. Bob Hunsberger, Wallenstein Feeds, Hog Economics Summary Sheet shows this change from eight weeks ago, profitability going from per pig with average production loss of (-$30.23) to profit per pig with average production of $27.93. A $58.16 per pig rocket increase in revenues. Then with the next twelve-month projection moving from (-$5.11) to $18.05. Seems to qualify as a reversal of fortunes.

From Canada Market Report_August 10, 2020

Again Bob Hunsberger, Wallenstein Feeds, Hog Economics Summary Sheet shows little in the way of encouragement or change from eight weeks ago, profitability going from per pig with average production loss of (-$37.90) to loss per pig with average production of (-$30.23). A $7.67 per pig increase in revenues that for some at least only says “you’re not bleeding as fast”. Then with the next twelve-month projection moving from (-$6.52) to (-$5.11). Arguably moving in the right direction but hardly comforting. Seems time for a better mousetrap

From Canada Market Report_June 15, 2020

Bob Hunsberger, Wallenstein Feeds, Hog Economics Summary Sheet shows little in the way of encouragement from eight weeks ago, profitability going from per pig with average production loss of (-$44.43) to loss per pig with average production of (-$37.90). A $6.53 per pig increase in revenues that for some at least only says “you’re not bleeding as fast”. Then with the next twelve-month projection moving from (-$17.61) to (-$6.52). Arguably moving in the right direction but the promise to just lose less money hardly something to get enthused about. Let’s hope the cavalry shows up with next week’s USDA June Hog & Pig Report or there’s going to be a lineup on liquidation.

From Canada Market Report_April 20, 2020

Bob Hunsberger, Wallenstein Feeds, Hog Economics Summary Sheet shows the reversal of fortunes in just the three weeks, profitability going from per pig with average production profit of $11.29 to loss of (-$44.43) per pig with average production. A $55.72 per pig decrease in revenues in just three weeks! Then with the next twelve-month projection moving from (-$3.13) to (-$17.61). Certainly not providing anything in the way of encouragement

From Canada Market Report_February 24,2020

From OMAFRA Monthly Hog Market Facts – Net Returns Farrow to Finish 2019

- January (-$29.79), February (-$33.43), March (-$27.16), April +$36.50, May +$47.33, June +$29.96. First 6 months $3.90

- July +$6.27, August +$22.33, September (-$32.26), October (-$25.54), November (-$27.84), December (-$30.09). Year 2019 (-$5.46)

Present_November 30, 2020

From OMAFRA Monthly Hog Market Facts – Net Returns Farrow to Finish 2020

- January (-$29.41), February (-$33.56), March (-$17.72), April (-$39.83), May (-$7.67), June (-$50.11). First 6 months (-$29.72)

- July (-$54.42), August (-$38.33), September (-$10.94), October ($22.36), November_N/A, December_N/A. Year 2020_(N/A)

In the words of Yogi Berra “Déjà vu, all over again”. Six months blackout of twenty-one. Granted these are averages but “on average the river is four inches deep, however you can drown in the middle”.

Tough business, not for the faint of heart. So, to the warriors I wish you all