Latest US Hog and Pig report meets analyst expectations, says AFBF

The US June Hog and Pig report contains few surprises according to analysis conducted by the American Farm Bureau Federation (AFBF). 6 July 2021

6 July 2021

3 minute read

3 minute read

By:

By: Last week, USDA’s National Agricultural Statistics Service released its latest Quarterly Hogs and Pigs report, providing a detailed inventory of breeding and marketing hogs as of June 1. Producers use this data to determine production and marketing strategies, while the industry uses it to assess the markets and the future supply of product.

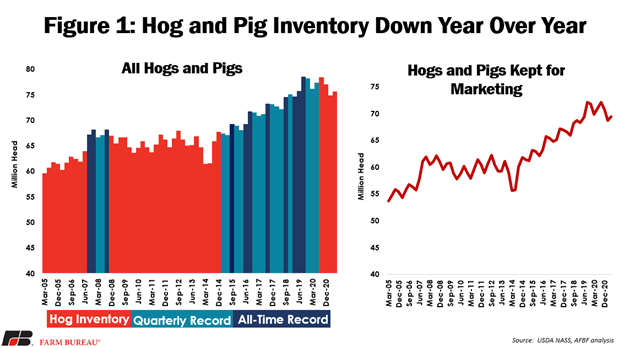

Hog and pig inventory

The report showed that on 1 June, all hogs and pigs were down to 75.653 million head, a decline of 2.2% from the same time last year. This decline was largely in line with expectations as analysts had been expecting on average a decline of 2.5%, with the estimates ranging from a decline of 3.5% to 1%. This decrease was the first year-over-year decline for June since 2014, when the industry was disrupted from PEDv.

This report also breaks a six-year streak of record levels of animals for the June report. The number of market hogs also declined by 2.3%, with USDA reporting 69.423 million head. This decline was also in line with analysts’ predictions, with pre-report expectations coming in at a 2.6% decline, with a range from a 3.7% decline to a 0.9% decline.

When looking at market hogs by weight groups, every weight group experienced a year-over-year decline. Lighter market hogs fell by larger percentages than heaver animals; market hogs under 50 pounds fell by 2.9% to 21.474 million head, and market hogs in the 50-119-pound range fell by 2.7% to 19.349 million head.

This contrasts with market hogs weighing 120-179 pounds falling by 1.5% to 15.010 million head and market hogs over 180 pounds falling by 1.5% to 13.589 million head. The breakout in weight categories was counter to the pattern analysts expected. Analysts were expecting greater declines in the heavier animals, forecasting declines of 4.4% and 5.6%, while expecting smaller declines in lighter animals with forecasts hovering around a decline of 1%.

This indicates that the industry is still working through heavier pigs more than analysts were expecting. This news could be short-term bearish for the market because it indicates that we have more market hogs ready for slaughter than we thought, which could also trickle down into pork supplies.

Breeding herd and pig crop

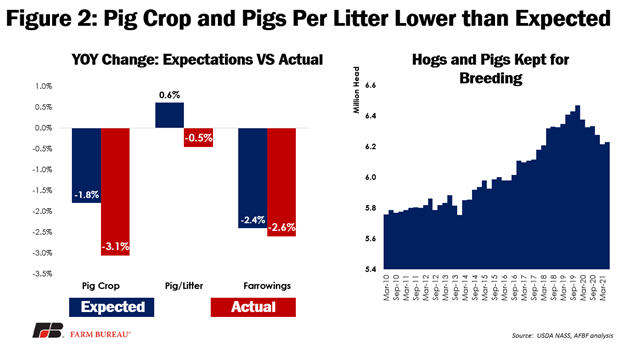

Prior to the report, analysts were expecting the June level of hogs kept for breeding to decline by 1.4%. This report fell right in line with this expectation, coming in at a decline of 1.5%, bringing the breeding herd down to 6.230 million head.

Analysts had forecasted an average 2.4% decline in farrowings for March-May, and this report delivered with a 2.6% decline to 3.067 million. The pigs per litter for this report was the primary surprise to analysts. Analysts had forecasted an average increase in pigs per litter of 0.6%, but instead this report revealed a decline of 0.5%, the opposite direction of analyst expectations and at the very bottom of the range.

Average pigs per litter fell from 11 pigs per litter at this time last year to 10.95 pigs per litter in 2021. This decline in the pigs per litter is the first decline for the March-to-May period since 2014. We can examine this data by month, and when looking at pigs per litter, the March number came in at 10.66, which is much lower than current trends. April pigs per litter was reported at 11.05 and May was 11.16, meaning that the quarterly average was really brought down by that March number.

When combining the decline in the number of pigs per litter with the decrease in overall farrowings, the pig crop for March to May dropped a steep 3.1% to 33.584 million head. This is compared to a forecasted 1.8% decline by analysts, and just outside the lower end of the range of a 3% decline. There are still industry reports of PRRS and this is likely playing a part in producer productivity and contributing to this decline in pigs per litter.

Moving on to the rest of the year, farrowing intentions are expected to decline at a greater rate than analysts anticipated. Analysts had anticipated both the June-to-August intentions to decline by 3.3%, with the actual intentions dropping by 4.4%, outside of the lower end of the expected range. September-to-November intentions were forecasted to decline by 1.2%, but instead, dropped 1.8%, to 3.084 million head, still within the expected range. When combining these lower intentions with the struggles in pigs per litter, we may be looking at reduced hog supplies and reduced slaughter levels as we move forward throughout the year.

Conclusion

The decline in inventory numbers indicated in last week’s Quarterly Hogs and Pigs report was largely in line with industry expectations, making for a neutral reading of the report. The report showed that on 1 June, all hogs and pigs were down to 75.653 million head, a decline of 2.2% from the same time last year. This decrease was the first year-over-year decline for June since 2014, when the industry was dealing with PEDv.

There was at least one or two surprises for analysts in this report. Analysts had forecasted an average increase in pigs per litter of 0.6%, but instead this report revealed a decline of 0.5%, the opposite direction of analyst expectations and at the very bottom of the range. Average pigs per litter fell from 11 pigs per litter at this time last year to 10.95 pigs per litter in 2021.