Pork Commentary: Snapshot US Industry

US - Nothing like a few months (seemed forever) to get a huge correction in the swine economic equation, writes Jim Long. 26 November 2013

26 November 2013

2 minute read

2 minute read

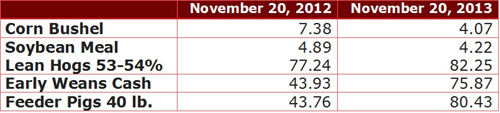

The huge drop in feed costs have decreased cost of production by $30 per head. This is now reflected in the price of early weans and feeder pigs. The $30 in lower feed cost has gone directly to the sellers of small pigs.

It appears at current feed prices, lean hog futures and good production the next twelve months will give farrow to finish operations a profit of $30-35 per head. The profitability is needed, Iowa State University estimates returns for farrow to finish per head had losses between $20-50 per head for ten months in a row beginning the summer of 2012 until the spring of 2013.

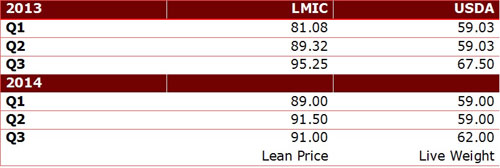

Price Estimates

Both the USDA and Livestock Marketing Information Center (LMIC) are projecting prices for 2014.

We expect lean hog prices will average above the USDA estimate for 2014. We see no indications that prices before September 2014 will be any lower than 2013. We believe the lack of breeding herd expansion and the continued losses from PED will keep hog supplies very close to 2013 levels.

Red Meat Production (Billion lb.)

The USDA is estimating US Beef Production will decrease 1.45 billion lbs. in 2014. That’s a huge decline. The USDA is projecting pork production to increase in 2014. That’s a huge decline. The USDA is projecting pork production to increase in 2014. We are not convinced this will happen to the extent they are projecting. The USDA projects 2013 will produce about 130 million lbs. more pork in 2013 than 2012. As of mid-November, actual ytd US pork production is about 200 million lbs. lower than 2012 (1.2 per cent). That’s 330 million lb. spread between projections and actual YTD. We cannot comprehend that the US pork Industry next year will jump 1 billion lbs. in production as the USDA Projects.

Capita Consumption

In the 1980’s US per capita consumption of Beef was 81 lbs. In 2007 it was 62.7 lbs. In 2014 the USDA projects per capita beef consumption at 50.7 lbs. Despite recent record high beef prices the cattle industry has not been able to make money. The LMIC reports that US cattle feedlots have lost money 9 of the last ten years. No wonder beef supply is collapsing. Without profits no industry can prosper and ever sustain itself.

Pork per capita consumption is projected to the summer. 44.4 lbs. in 2014. US per capita consumption of boneless equivalent has never exceeded 50 lbs. Reality is pork per capita consumption has hovered between 43-49 lbs. for the last 100 years. We have held consumption per capita but haven’t grown. It’s a real challenge and opportunity to get demand such that our industry can grow with increased per capita consumption while still achieving sustained periods of profitability.

Summary

No doubt the tide has turned for our industry. Reasonable profitability is present and will be here at least through the summer. In our opinion the fall of 2014 still looks promising for profitability. We still Believe there has been next to no sow herd expansion, we expect pork demand both domestically and globally to stay strong. We all need a chance to make some real money.