China: Hog Markets

CHINA - Looking at the size of the breakdown of the inventory for November, 2013-breeding stock was around 50.33 million sows and total on farm inventory was around 458.75 million (as compared to October 2013-breeding stock was around 50.58 million and total on farm inventory was around 457.83 million, writes Ron Lane, Senior Consultant for Genesus China. 23 January 2014

23 January 2014

5 minute read

5 minute read

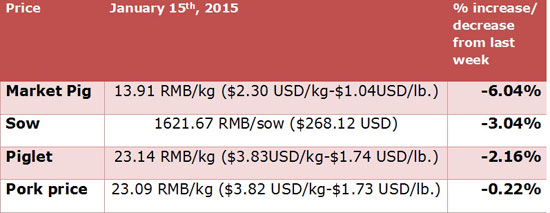

The 458.75 million head for November is up 0.7 per cent from last year while the November sow inventory of 50.33 million is down 2.3 per cent from last year (year over year). Profit margins are now showing large reduction yet still positive returns. On 15 January 2014 it was reported that profits for a farrow to finish operation was 49.06 RMB/market pig ($ 8.11 USD/market pig). This is down by 96.01 RMB/market pig ($ 15.87 USD) from the week before (a 66.18 per cent decrease in 1 week). This time last year, the estimated profit was 382.23 RMB/market pig ($63.20USD/market pig); this year 49.06 RMB/market pig ($8.11 USD/market pig) (this is a 333.17 RMB ($55.08 USD) drop or an 86.94 per cent drop in profit). At the end of April, the estimated national losses were around 139 RMB/market pig ($ 22.98 USD/market pig) (as compared to the end of March when losses were 260 RMB/head ($ 42.99 USD/head). For the past 25 weeks, there has been reasonable profit for the pig farmers.

Last week (15 January 2014), the pig to grain ratio was 6.18:1. This fell from 6.52:1 from the week before (a drop of 5.27 per cent). At the end of October, the pig to grain price ratio was 6.59:1. This compares to the end of September pig to grain price ratio of 6.53:1; June monthly average of 5.76:1 and May monthly average of 5.28:1. One year ago on 13 January, the ratio was at 7.52:1). On the whole, in 2013 the national average of pig grain price ratio was 6.15:1 as compared to 6.25:1 in 2012 ( fell by 1.6 per cent). The chief reason was related to the pig market losses of more than five months during the spring and summer of 2013.

On January 15th, 2014, the average corn price was 2.31 RMB/kg or $0.38 US/kg or 0.17US/lb. This is down 0.83 per cent from last week. The retail price to farmers for soybean meal would be 4.18 RMB/kg or $0.69 US/kg or $0.31US/lb. The national average wheat bran price was $2.03 RMB/kg ($0.34US/kg or $0.15US/lb.).

According to the Beijing 15 January news, traders reported that the Chinese quality inspection department (AQSIQ) refused the entry of ships carrying US corn DDGs. The reason was cited that the shipment contained GMO (MR 162) that did not have the approval of the Ministry of Agriculture (MOA). This was not expected by the traders since a week ago, rumours in the market place suggested that China had relaxed the quality inspection checks on US DDGs. (state media reported that authorities had rejected 601,000 tonnes of grain in 2013. Since then, other loads including this one have also been rejected).

Heavy rains last fall that led to flooding in the North-east province of Heilongjiang have affected the domestic soybean crop and thus yield and quality for harvesting. Not only will the soybean harvest be less than 12 million tonnes, the rising need for imports mainly for animal feed proteins will be increased. In 2012, China imported nearly 60 million tonnes. For this crop year, previous forecasts pegged the soybean imports at 65-67 million tonnes, but with the current flood damage, imports could reach nearly 70 million tonnes. Government reserves have been offered for sale, but the low quality of the stored beans has resulted in limited sales. China’s soybean imports are expected to grow by 9 to 13 per cent for this crop year. (Estimated grain imports of 13.98 tonnes and 58.38 million tonnes of soybeans has been reported for 2013 for China).

Who wants to export pork products to China? Mexico has signed a trade agreement with the Chinese Government to export pork products, mainly offals to China (must be ractopamine free). Recently, Chinese representatives announced that two Danish Crown companies can soon export processed meat products (the first in the world) to China. The main reason that this is happening is that these two companies (Tulip and Danish Crown) have a strong focus on food safety. The Russian meat processor- Miratorg, first shipped pork products to Asia in 2011.This year, the company projects that they will ship about 2,885 tonnes of pork to Hong Kong and will increase sales to about 3,838 tonnes of pork for the first six months of 2014 into Hong Kong. Miratorg sees other Asian countries such as mainland China and Viet Nam as areas for good demand for their products (Genesus supplies swine genetics to Miratorg). And then there is Shaunghui International Holdings. Shuanghui has become the world's largest pork supplier with access to nearly 40 million slaughter pigs (25 million from Smithfield and 15 million from their own Chinese suppliers). What products from this source will start to enter the China market place?

It is estimated that during the 3rd quarter of 2013, the total national pig slaughter reached 173 million head an increase of 0.6 per cent from last year. If one looks at the large scale processors (fixed-point slaughter), then these facilities slaughtered 165 million head for the first 9 months of 2013 (an increase of 4.7 per cent year on year). During the 3rd quarter, these plants slaughtered 57.8 million head, an increase of 6.5 per cent from 2012. With the focus on food safety, more of the pigs will be marketed from highly regulated slaughtering and processing plants.

According to Custom’s statistics, 430,000 tons of pork (an increase of 7.83 per cent from last year) has been imported into China during the first 9 months of 2013.

The Consumer Price Index (CPI) is quite interesting for the National Government. Rising food prices and especially increasing pork prices greatly affects the CPI. The CPI is made up of 30.49 per cent food found in the consumers’ basket. Pork is estimated to be about 1/3 of the food portion of the basket or in other words, about 8 to 10 per cent of CPI as a whole. CPI for China in December was 2.5 per cent, a seven month low. November was 3 per cent-a 3 month low (September was 3.1 per cent and for October it was 3.2 per cent). Overall inflation for 2013 was 2.6 per cent, which is lower than the national target of 3.5 per cent. Food inflation was 1.33 per cent for December (1.92 per cent for the November inflation growth).

| Genesus Global Market Report Prices for the week of January 13, 2013 | ||

|---|---|---|

| Country | Domestic price (own currency) | US dollars (Liveweight a lb) |

| USA (Iowa-Minnesota) | 168.99 USD/lb carcass | 125.05¢ |

| Canada (Ontario) | 158.75 CAD/kg carcass | 52.11¢ |

| Mexico (DF) | 26.6 MXN/kg liveweight | 90.67¢ |

| Brazil (South Region) | 3.84 BRL/kg liveweight | 73.81¢ |

| Russia | 75 RUB/kg liveweight | $1.00 |

| China | 12.77 RMB/kg liveweight | 95.78¢ |

| Spain | 1.211 EUR/kg liveweight | 74.55¢ |

| Viet Nam | 48,000 VND/kg liveweight | $1.03 |

| South Korea | 3,508 KRW/kg liveweight | $1.49 |