CME: US Meat Export Pace Slowing

US - Export data for November, released by USDA, confirmed what many in the industry already knew—the pace of meat exports has slowed down and it is now tracking below year-ago levels, write Steve Meyer and Len Steiner. 9 January 2015

9 January 2015

3 minute read

3 minute read

By:

By: In the case of pork, exports have declined sharply and likely have contributed to the recent price declines. Below are some of highlights:

Pork

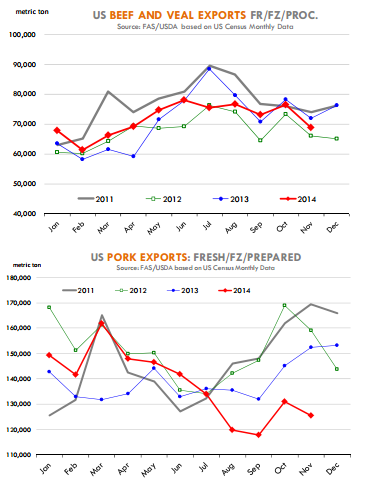

US pork exports declined for the first consecutive month in November and at 17.7 per cent, the decline was the biggest year/year drop since March 2013. Total shipments of fresh/frozen/processed pork were 125,377 metric tons (MT), the smallest November export volume since 2008.

A number of factors likely contributed to the decline in pork exports. High prices over the summer and early fall caused traditional buyers of US pork to look elsewhere to fill their needs. And it became increasingly easier to find alternatives given the gains in the value of the US currency and lower pork prices for European and South American products.

Exports to Japan at 25,901MT were down 22.3 per cent and they have declined 20 per cent in the last three months. Mexico has been quite aggressive in buying US pork so far this year as PEDv loses there forced buyers to source product in the US market despite the higher prices. Still, shipments to Mexico in November were 40,988MT, down 8.9 per cent from a year ago. Export to China have fizzled, with exports in November a mere 3,186MT, down 77 per cent from a year ago.

US pork exports should rebound in Q1 but lower prices are needed to offset the currency impact and also “buy back” the market share lost to our competitors.

Beef

Total exports of fresh/frozen and processed beef in November were 68,784MT, 4.3 per cent lower than a year ago. Despite the decline, beef exports have held up better than most expected so far this year, largely because of exceptionally strong demand in Asian market. Japan is the top market for US beef and exports to that market in November were up four per cent compared to a year ago.

In the past three months, exports to Japan have increased 19 per cent, an increase that is even more impressive given the surge in the value of the US currency. Exports to other Asian markets were somewhat mixed. Shipments to South Korea in November were 10,495MT, 41 per cent higher than a year ago while exports to Hong Kong, a growing market in 2013 and early 2014, were 13,253MT, down 12 per cent from last year.

Despite the decline in exports to Hong Kong, this market remains very important for US beef trade, helping US packers capitalise on the growing demand for beef in China. Beef exports to Hong Kong in 2011 averaged a little under 4,000MT a month and in 2012 they were still around 5,300MT per month.

Exports have increased sharply in the last 18 months as China has emerged as a very large global beef buyer, bidding on product from South America, Oceania and (via Hong Kong) North America.

It remains to be seen how exports to this market will progress in 2015, especially since Brazil now has been granted access to the Chinese mainland market. While beef exports to Asia generally remain robust, shipments to our North American partners slowed down in November, with exports to Mexico at 9,504MT down 16 per cent from last year and exports to Canada at 9,566MT down 11 per cent from a year ago.

Despite the most recent decline in shipments to Mexico, overall exports there have performed quite well so far this year, especially considering the impact of a weak Peso and high prices for all meat proteins in Mexico.

Monthly shipments in 2014 have averaged about 11,600MT compared to 10,768MT per month in 2013 and 9,372MT per month in 2012. Exports to Canada, on the other hand, are off significantly, down about 21 per cent for the year. In all, we think that beef demand in export markets remains quite robust.

So far, the surge in the US dollar appears to have had a limited impact but it remains to be seen how beef exports perform in the coming months given slowing global growth.