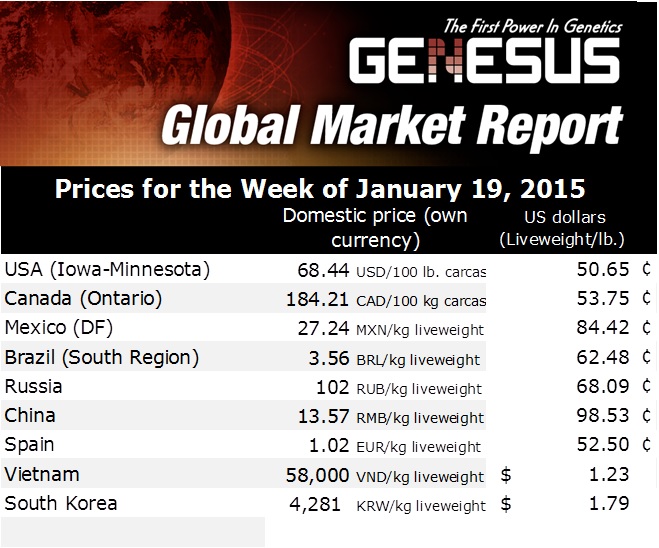

US Hog Markets

US - Although it is still early in the year, some market analysts are starting to talk about hog weights for 2015. Everyone has an opinion, so here is mine, writes Alan Bentley, Sales & Service for Genesus USA. 30 January 2015

30 January 2015

2 minute read

2 minute read

By:

By: Two things will dictate weights for 2015. The first is the price of corn. Lower corn prices will keep weights at or near last year’s level, and it is easy to understand that premise's supporting logic.

Feed costs are not the only factor that dictates carcass weights. Packer’s grids also influence at which weight producers sell their animals. The move to encourage heavier carcass weights has been going on for nearly 40 years, and I do not see this trend changing. Most of the grids I see are enticing producers with higher premiums to take them to 285 pounds (live).

There has always been an argument that the export market likes smaller portions. My contention with that has always been that a consumer can create smaller portions with a knife. Packers have a certain amount of fixed costs. If a plant killing 8,600 head per day adds just two pounds on to each carcass, that equates to approximately 17,200 lbs. of additional meat every day. Most importantly, their fixed costs did not change.

We as producers utilize barns in the same way. As long as the packer will pay for larger carcass weights and producers can put it on for less then what the packer is willing to pay for it, then we will. There could be an argument whether or not there will be enough finisher space. I will bet, however, that the hog producers will figure out how to get it done.

Oil prices falling and the United States Dollar advancing will make exports more expensive for the rest of the world. With cheaper gas, we should have additional funds available to buy more meat. That will be unless the Federal Government decides to start raising interest rates. With a high average debt per American household, I believe some of the money saved at the gas station will be used to pay the interest on debt.

Using many of these same arguments, feed should remain affordable. Burning our food has tied corn prices to oil. With oil below $50/barrel, corn prices' upside potential should be limited. The corn producers have locked up the bins, but end users still know it is there and eventually will have to be sold. Payments still have to be made, and the key to those locked bins will have to be found. Good weather should also keep corn prices manageable.

One final comment to make about pork’s price at a retail level is it with comparison to chicken and beef. We are at or near record low levels when compared to beef, and we are at or near record high levels compared to chicken. We need to concentrate on making sure the public understands our value, as compared to beef. Chicken, can stand on its own.

In reflection on the above commentary and the industry overall, we lost a good “hog man” on January 10, 2015 when Bruce Hild from Neligh, Nebraska passed away. I would like to dedicate this commentary to Bruce. He was one of my biggest influences in this business. He forgot more knowledge and insight of the hog industry than I will ever know. Not only will Bruce be missed by his family and friends, he has a large hog family that will also miss him dearly. Thank you Bruce for teaching me all that you did! You will be forever remembered.