CME: High US Pork Availability Led to Price Decline

US - Comparisons of the 2015 pork market with 2013 pre-PEDv levels show the impact of increased domestic availability on prices, write Steve Meyer and Len Steiner. 30 March 2015

30 March 2015

3 minute read

3 minute read

By:

By: We covered the estimates of the upcoming USDA Hogs and Pigs report in our Wednesday letter but, as market participants focus on the numbers this afternoon, we thought it was important to bring some context to the numbers.

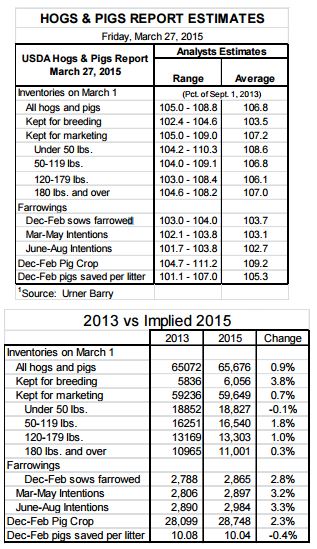

The survey of analysts polled by Urner Barry shows big increases in almost all categories of the report, creating the impression of a dramatic supply expansion in the US pork market.

After all, 1 March inventories are expected to be up 6.8 per cent and the pig crop in the first half of this year is expected to increase by as much as 9 per cent compared to last year.

The key fact to remember, however, is that these numbers are higher than last year, and 2014 was anything but a normal year.

More than half of the US breeding herd was infected with PEDv causing the death of millions of baby pigs. Concerted efforts by industry and government have allowed US hog producers to recover and current inventory numbers have now returned to levels prior to the PEDv outbreak.

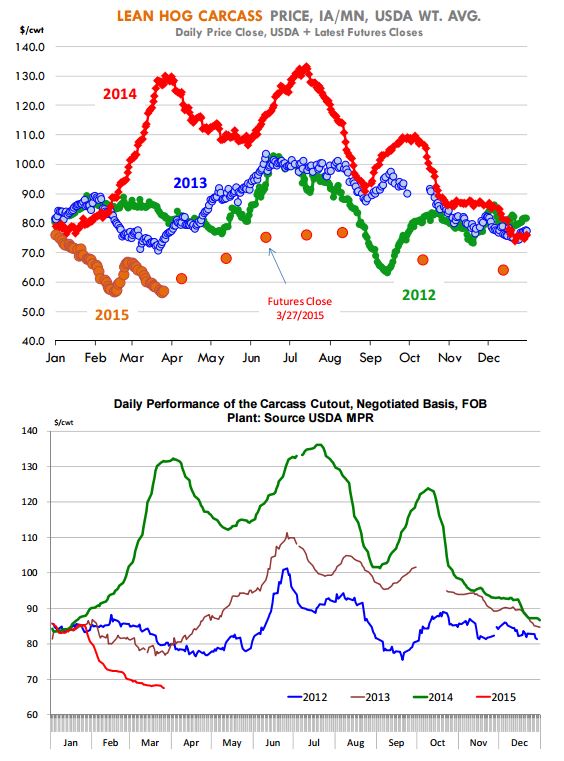

Based on analyst estimates, the Hogs and Pigs inventory as of March 1 is expected to be about 65.676 million head, less than one per cent higher than 1 March 2013. And yet, current hog prices in the cash market are down some 24 per cent compared to the same time in 2013.

If one only looked at the futures markets, and nothing else, the conclusion would be that there is a glut of pork in the domestic market. And yet, we have only slightly more hogs on the ground at this time than we did in 2013.

So if hog supplies on the ground only imply recovery from the deep hole of 2014 and back to levels we saw in 2013, why are cash hog carcass prices down in the 50 cent range compared to mid 70s back in 2013?

A number of factors are presented as contributing to the precipitous decline in hog prices. Pork exports were down 20 per cent in January and, based on the weekly pork export reports, they were down another 15 per cent in February and likely down 5 per cent in March (this is not the USDA estimate just our best guess using weekly exports).

This would imply a Q1 pork export number of about 1.150 billion pounds, down 14 per cent from a year ago but down just 5 per cent compared to exports in 2013. Compared to 2013, the decline in exports in Q1 represents about 62 million pounds.

A very strong US$ and lower prices in competing markets (especially Europe) will be much more challenging in 2015 than they were in 2013. We might export a similar volume of product but lower prices will be needed to accomplish that. Keep in mind that sales do not equal demand.

The second issue to consider is the changes in production not just slaughter. While hog inventories as of March 1 are only 0.9 per cent of what they were in 2013, pork production in the quarter is expected to be about 5.3% larger, mostly due to heavier carcass weights.

The average hog carcass weight in 2013 was 207.3 pounds. In Q1 of 2015, hog carcass weights are expected to be around 215 pounds. The eight pound difference implies an additional 223 million pounds of pork in Q1 or about 4 per cent of production.

Larger production levels, lower exports and an increase in pork imports (largely from Canada) have increased pork availability in the domestic market. Per capita availability (on a carcass weight basis) in Q1 of 2015 will likely be up about 9 per cent compared to the levels we saw in 2013.

This kind of increase is indeed significant and helps explain a good part of the recent decline in prices.

At this point futures have built in a 25 per cent discount to hog prices in late spring and summer of 2013. What could change the level of that discount is an improvement in export demand (lowering domestic availability) and a reduction in hog weights.

Pork inventory numbers show dramatic increases from 2014 but export demand, carcass weights and ultimately per capita availability deserve more attention.