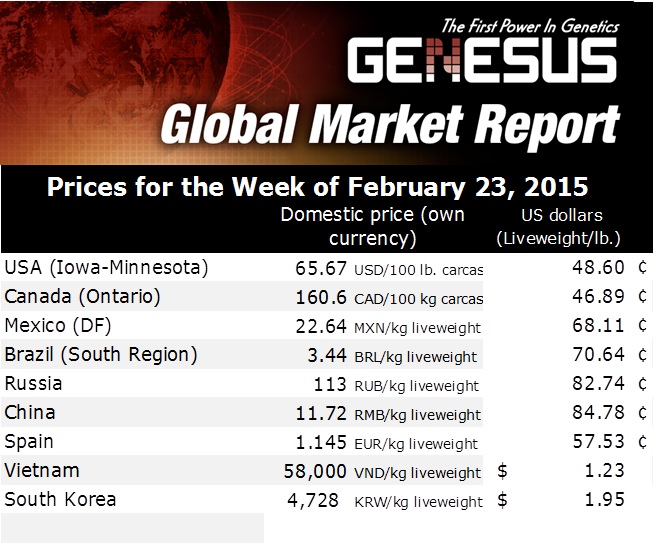

Spain Hog Markets

SPAIN - After 26 weeks of hog prices dropping all around the EU, the last week of January saw this trend break and penny to penny has gone up from €1.030/kilo liveweight to €1.125/kilo liveweight in the market of Mercolleida, the Spanish reference market, writes Mercedes Vega, General Director for Spain, Italy and Portugal. 5 March 2015

5 March 2015

3 minute read

3 minute read

By:

By: Last week, the price in Germany rose seven cents, going up to €1.14€. The bottom-line is that the hog price has increased in the whole European continent and most importantly it has been in a most significant way compared to the lowest numbers recorded early 2015. It has been many months with values below the cost price of production throughout EU.

The price turnover has been reached thanks to different factors. First of all it was due to the sharp fall of the euro against the dollar (it has dropped by 17 per cent from a year ago) which has given the EU the competitiveness to export.

Secondly, it was also due to a lower supply of pigs. Also, pigs were lighter compared with the previous period. There were plenty of heavier hogs after Christmas.

In contrast, domestic pork consumption is still steady; having fallen a little across the EU by two per cent, including Spain, although in the last three months it seems to be improving slowly.

As opposed, the situation of Spanish export, compared with the drop of 140,000 tons exported to the EU, referred to the 2013 crisis (Russian ban could not be absorbed), Spain is again outperforming 1+ million ton (1,076,365 t) of storaged pork between frozen and fresh, representing a 9.3 per cent increase over 2013 and a value of €2,547 million (+ 8.3 per cent compared to 2013).

According to the ICEX-Estacom (Spanish Institute for Foreign Trade) Spain's pork exports have increased from 2009 to 2014 by 22 per cent in quantity and 52 per cent in value, as shown in the following graph.

Increase in Production

Production in the EU has increased slightly, mainly due to the higher efficiency of sows.

According to the last Spanish swine herd/inventory, on December 31, 2014, it has increased by 105,000 heads to reach 2.36 million sows, representing an increase of 4.7 per cent from a year ago and exceeding 26,5 million head of hogs which means an increase of 4.1 per cent.

This increase of animals is given by the greater number of sows and the improving productivity due to better genetics. In other words, these figures mean an increase of 1 million heads per year. It is the first herd increase since the feed crisis in 2007.

In Portugal, there has also been an increase of 4.2 per cent, to 2.1 million heads on its total pig inventory. The sow inventory is a little higher with 231,000 sows, indicating a herd increase of 3.6 per cent compared to 2013.

Regardless, the hog price in Portugal has followed the same path as the EU and especially Spain. It has increased in the Bolsa de Montijo do Porco in the first half of February, giving an increase of €0.06/kg carcass (trend Canal E 57 per cent).

Portugal also increased its pork importation from Spain with an upturn of 7,200 tons in 2014 which means seven per cent more than in 2013. Thus becoming the second largest importer of Spanish pork and leaving Italy in third place with 115,457 tons of pork.

Both Portugal and Italy account for 11.7 per cent of Spanish pork exports and Portugal’s imports account for the 27 per cent of Spain’s domestic consumption.

FIGAN

On another point, from March, 17 to 21, the Spanish Animal Production Trade Show (FIGAN) will be held in Zaragoza. It is the most important international trade show of the Iberian Peninsula.

Genesus will be attending the show with a representative booth and in line with our international image. We would like to invite all of you to be part of what we are going to offer during the show.

On Wednesday 18 11:00 AM, Genesus is putting on a presentation about The Pig of the Future and its Profitability. This will allow us to introduce Genesus to the market and make available to all hog producers our genetics and our technology.