UK Pig Prices Down at End of February

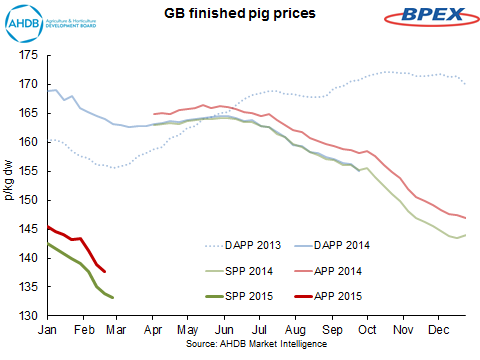

UK - At 133.21p per kg, the EU spec GB SPP for the week ended 28 February was down 0.74p on the week. 6 March 2015

6 March 2015

1 minute read

1 minute read

By:

By: While a continuation of the downward trend, this is the smallest weekly decrease recorded since the turn of the year.

The extent of the current drop in price, however, has reached almost 10p since the beginning of 2015, a third of the difference compared with the DAPP at this time last year.

With reports that recent spot market prices have been slightly more positive, alongside some increasing European finished pig prices, it is possible that, whilst not yet a turn around, the slow-down in price reductions could be sustained.

Aiding this, although estimated slaughterings were up slightly on last week, there are signs of the normal seasonal tightening of supplies. In addition, average carcase weights at 82.7kg, the lowest of 2015 so far, should halt supply from running any further ahead of demand.

The EU spec GB APP in the week ended 21 February was 137.69p per kg, down 1.25p on the week. The gap with the SPP for that week narrowed slightly to 3.74p/kg.

With uncertainty still apparent in short-term finished prices, the weaner markets remain unpredictable, with changes in the number and mix of animals being marketed influencing price levels. In the week ending 28 February, 7kg weaners moved up 42p to £33.83 a head, while 30kg weaners dropped £1.21 to £44.82 a head.

In part offsetting the previous week’s increase, 30kg producers are now receiving over £12 less than last year’s prices, while 7kg quotes remain around £8 down on the year.

Read more in the AHDB BPEX Pig Market Weekly report.