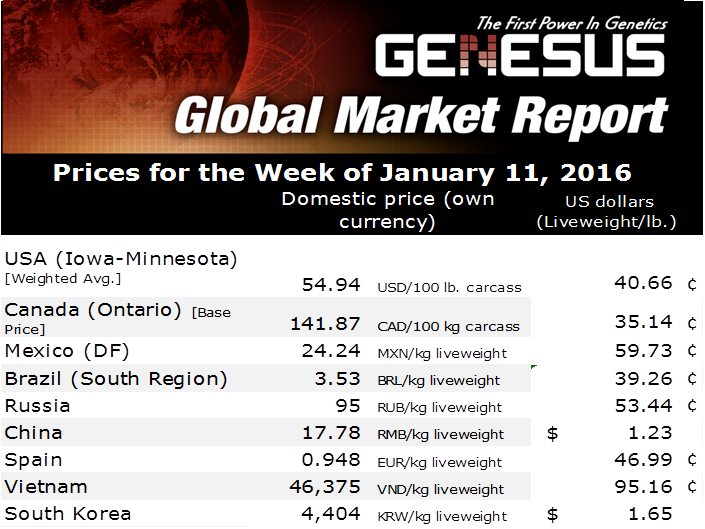

EU and Spanish Pork Markets

SPAIN and EU - Spain’s slaughter numbers went up 7 per cent in 2015 compared with 2014. Spain exported 45 per cent of its pork production (Germany and Spain have increased their exports, while other EU countries have declined), also heavier slaughtering weights (112kg average), writes Mercedes Vega, General Director for Spain, Italy & Portugal. 25 January 2016

25 January 2016

3 minute read

3 minute read

By:

By: The price average was € 1.14/kg liveweight, but with the lowest price at the end of the year at € 0.947/kg, while the price of feed more or less stabilized, with an index at the end of the year of 225 € / ton (source 3tres3 pig economic thermometer).

Besides the small pig price was below breakeven, causing disruptions for many producers who either have been integrated into larger structures and some of them have quit as producers. This meant that fewer pigs will be available.

At the end of the year Spain’s price has an average above Germany’s (1.14 versus 1.08 € / kg) but ends the year with a price below that (0.947 compared to 0.97 € / kg live weight). With an inventory that in Germany got down by 3 per cent, with 27.4 million head (data from November 2015, the lowest since November 2011 inventory) versus a sows inventory felt at 4 per cent. While Spain continues to rise by 2.3 per cent in sows and 6.2 per cent in total, reaching 26.98 million head (official data from the Ministry of Agriculture, Environment and Food Spanish May 2015, MARMA).

Spain’s domestic consumption has increased by 2.2 per cent in fresh meat at expenses of 2 per cent in processed meat, (48.8 kg in 2014 vs. 59.9 kg in 2005, according with MARMA). Having say that we couldn’t say that the market in Spain doesn’t look the best for this year.

The weights have increased, have been overcome the 88 kg in carcass weight and 114 live weight.

This is also creating a problem for small pigs, there is basically no place in finishing barns.

Something to highlight it is the good job and efforts made by the industry to open new markets.

One of the “new” sectors that has worked very well has been sales of Iberian pork by opening new markets, promoting meat quality in Asia. By the way, last week, Extremadura Region got an Asian delegation interested on importing Iberian pork.

Also the inter-professional agri-food organism called INTERPORC has been very active by promoting Spanish pork in Asia. They got a lot of attention bringing specialized journalists and media to visit Spain and touring production and processing facilities all over the country.

The European market is stabilized in the hog market and it seems that picks up in the pork meat.

Until January 13 Germany had frozen 23 per cent of its production and Spain was requested to get frozen 22.8 per cent of it (Italy represents 4.4 per cent and Portugal 0.8 per cent). This amount represents 53.9 per cent boneless frozen meat. To date they have already locked over 60,000 tons.

PORTUGUESE MARKET

The market situation in Portugal ended with big problems. 2015 has been a year started good, but ended in a bad way with prices well below cost of production.

Carcass price, stood at year-end close of 1.00 € / kg carcass weight, which is about € 0.77 / kg live weight. At this price you have to deduct the cost of transport it has to assume the producer to slaughterhouse.

Over the last couple weeks the price has increased € 0.05 / kg carcass, but the recurrent campaigns made retail market level of up to 50 per cent off makes it impossible to increase producer prices. Meat is being sold below 1.00 € / kg to consumers, which is not helping the image of the product as safety and quality.

Throughout the month of December there have been awareness campaigns and information, from the Cabinet of Crisis of the Swine Industry to the Portuguese consumers, whether the meat they are eating is of Portuguese origin or not. This information is mandatory and must be included in the labeling.

ITALIAN MARKET

The reference price QUOTE OF THE CANAL "E" (EXTRA). EUR / 100 kg for Italy is 136 € over the last week of 2015.

Reaffirms its tendency to raise prices. Italian market shows a higher supply compared with its demand due to the number of animals slaughtered during the month of December have avoided delays after Christmas. There are fewer pigs, although heavier (having reached more than 171 kilos) and the trend appears to be continuing.