Pork Commentary: USDA June Hogs and Pig Report

US - The USDA June 1 Hogs and Pig Report was released last Thursday, writes Jim Long President – CEO Genesus Inc. 30 June 2016

30 June 2016

2 minute read

2 minute read

By:

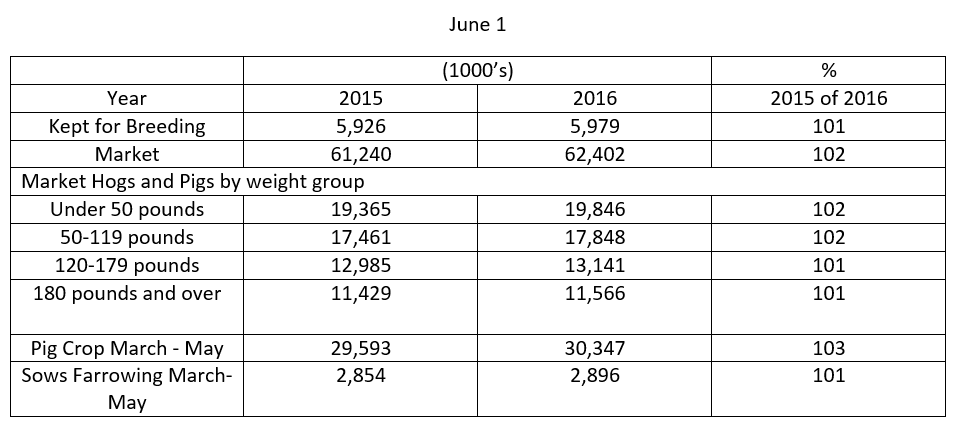

By: Breeding Herd

June 1 up 1% or 53,000 sows from a year ago. What’s interesting there is no increase in the breeding herd since March 1 (March 5,980 - June 5,979). If you have been reading our commentary we have written that there had been little expansion, as new sow barns are just replacing one’s going out of business.

Other Factors:

- Loose sow housing generally means less sows in the same space compared to gestation crates.

- Infrastructure age – many old sow farms that need updating. Cost prohibitive for many or just as importantly doesn’t make economic sense.

- Labour issues, producers tired of chasing labour.

- Agriculture wealth. There is lots of money in ag equity. i.e Iowa alone has $225 billion in ag equity. Some don’t need to bother with the 24/7 of sow production.

- Environment, getting barns permitted is a chore. The Not-In-My-Backyard (NIMBY)syndrome is prevalent in many areas making it difficult to get sow barns permitted. Farmers who grow grain you would think would want to have feed customers such as pig farms but are some of the biggest nimby opponents. The same farmers believe burning food (ethanol) is a long term business model. Reminds us “We have seen the enemy and it is us”

Bottom line

There will be new sow barns but when dust settles there will be not significant sow herd expansion. Take home – 6 million sow spaces, replace 2% for obsolesce, fire etc. retirement etc. a year. That’s a 50 year sow barn inventory turn. Need 120,000 new sow spaces a year at 2% per year replacement. No way we will build over 120,000 sow spaces a year in the foreseeable future.

Market

1% more sows have led to 2% more pigs. Not hard to figure productivity gains as an industry of 1% per year is not a surprise.

The Market inventory is 1.160 million more than a year ago. Let’s assume 25 weeks (175 day) birth to market. The increase averages 46,000 a week.

The National Hog Farm reports Packer capacity is currently at 2.496 million a week compared to 2.441 million last fall. The 46,000 a week increase estimate re. USDA should not be a problem. New Plant capacity by the end of 2017 could be 2.615 million a week. That’s 220,000 plus a week over current capacity and production. Need almost 500,000 more sows to fill those shackles and that’s not happening. In our opinion Packer margins will be good through the fall of 2016. After that Packers will look like farmers, couldn’t stand enough of a good thing.

There will be quite a battle for hogs to meet packer need, retail shelf space, export orders and food service demand.

Packers who have locked in hog supply will be at a big advantage.

Summary

Sow herd hardly changing, more market hogs coming. Fall 2017 we will trade dollars like most years.