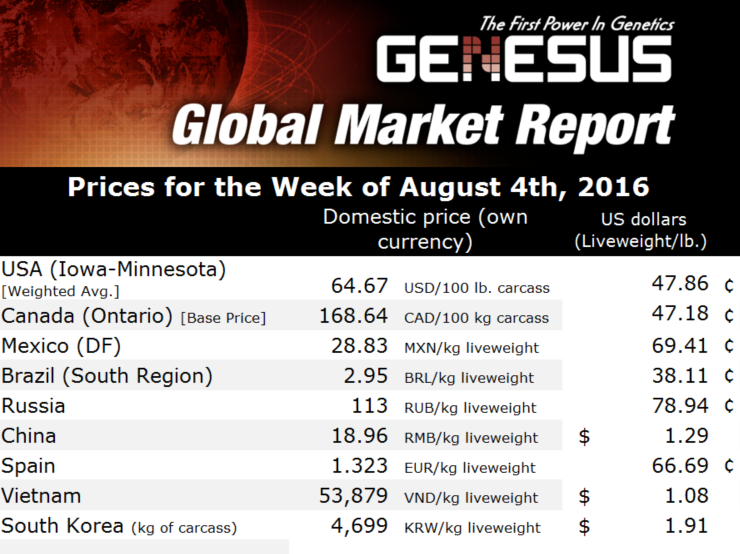

EU and Spanish Pork Markets

EU - After 15 weeks of sustained growth in Spain, the price has stalled over the past two weeks. The price came from 0.950 €/kg live weight in the first weeks of April (way below the production costs) to currently 1,323 €/kg live weight, writes Mercedes Vega, General Director for Spain, Italy & Portugal. 11 August 2016

11 August 2016

4 minute read

4 minute read

By:

By: The total increase has been of 39 per cent, being now above cost of production, however the annual average has been of 1.07 €/kg life weight, which does not reach that production cost. This spectacular increase is taking the price only 5 per cent above last year’s price, and barely compensates the losses experienced by the producers in the first months of this year.

.PNG)

Since the last week of June there is a lack of animals for “slaughter” in Spain and this is the case in all the EU. Although the hog prices have increased the industry has not been able to translate these increases to the value of the meat.

However, by having less animals with less weight there is less available meat. The contraction of the offer is normal during this period of the year due to the heat of the summer, however it has been exacerbated this year by the “strong” demand from China.

The lack of animals in all Europe combined with the decrease in the slaughter weight is an indicator that there is no speculation in this case. The producer has either to slaughter animals with less weigh to honour previous commitments with their clients, or to make room in the farms for piglets that are still coming regardless of the heat situation that prevent the animals from sustaining their normal growth process.

Differences are starting to arise between the slaughterhouses which are exporting to Asia, that have a sustained need for animals with appropriate weight and the slaughterhouses that are certified and export hogs to the European market. The first are benefiting from a strong demand and from prices on the rise, while for the others the demand is not homogeneous and prices have already reached their maximum.

This overall situation has resulted in some slaughterhouses taking the decision to slaughter four days a week, as has already happened in Germany. The contribution from the strong demand from China has been reducing significantly and this has resulted in a renewed interest to increase exports to their more familiar market of Portugal and France.

During the first quarters the weights have been way above the ones from previous years. However these have maintained the levels from the last two years, in line with the ones in France and Germany. When comparing the stronger producers in Europe (Spain, Germany and France) prices are now very similar, contrary to previous years when Spain clearly differentiated from the other countries during summer time.

Internal consumer demand in Spain and generally in Europe remains fragile, even more so during this time of the year. However in Spain, tourism has a positive impact on the consumption of cured and processes meat, but not of fresh meat.

When it comes to Spanish exports, the first five months of the year have been spectacular. The accumulated amount from January to May has already surpassed 900.000 Ton (23 per cent more than last year, an additional 170.000 Ton). Sixty-one per cent of these exports went to the European market and 39 per cent to other countries. That translates to additional 16.000 Ton to the EU (from 2 per cent to 5 per cent) and 110.000 Ton to other countries (around 70 per cent more).

Exports to China have triplicated in terms of meat as well as sub-products. As a result the Spanish exports mapping has changed significantly. China is now the first destination of Spanish exports before France. The resulting distribution of meat exports is now as follows: China 19 per cent, France 16 per cent, Italy with almost 11 per cent, Portugal 6 per cent, Japan 5.6 per cent and Korea and United Kingdom with 4 per cent each.

Portuguese Market

The price from the Montijo market has risen from 1.671 €/kg at the beginning of the summer to 1,826 €/kg the Carcass E 57 per cent at close last week, which has been the result of a price imposition.

The hogs are still at very low weights, a sign that the offer is below the demand. In any case, the concerns from the industry are that the sales of meat continue to be weak and they still cannot translate the increase of pricing to the consumer.

There is a lesser demand of hogs, as a result of both a decrease in internal consumption in Portugal and a stagnation of prices in the European market, mainly in Spain.

Italian Market

The Italian market is the strongest in the European market at this time. It has experienced strong prices increases and a sustained demand. There is low offer, but in comparison with the rest of Europe the demand is higher.

The strong consumption derived from tourism has allowed the translation of price increases of the live weight to the final consumer, which has not being the case for the rest of Europe. The quote at this moment for weights from 160/176 kg of live weight is 1,617 €/kg.