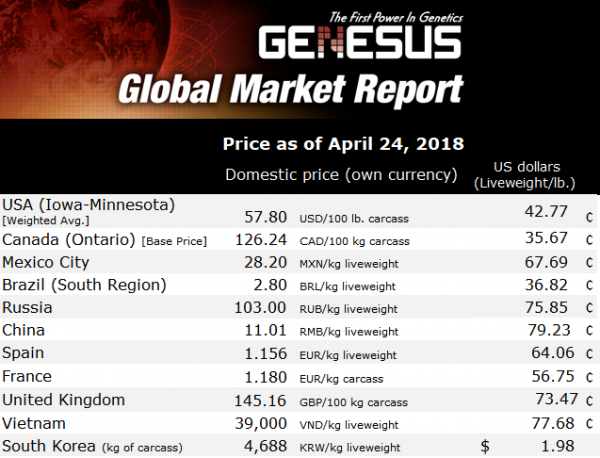

Genesus Global Market Report: Canada - Is the party over?

The recent NASS semi-annual pig crop for both the USA and Canada places the sow herds at 6.18 million head and 1.27 million head respectively. Inventories of all hogs and pigs are 73.2 million USA and 14.3 million head in Canada. 24 April 2018

24 April 2018

2 minute read

2 minute read

Bob Fraser – Sales & Service, Genesus Inc, [email protected]

This is a continuation of recent trends of moderate expansion coupled with the steady march of improved productivity leading to plus or minus 2% growth year on year for the last few years. Also Canada running at 20% of the American herd is a traditional long-term trend only rising perhaps to 25% early in the millennium. 20% seems to be the natural balance.

There always seems to be a certain angst as to whether we will be able to kill all the hogs but it appears new packing plants will help handle the additional volume of pigs in both countries. Whether by good luck or good management it seems we always manage to get all the pigs produced dead (at a price). Packer capacity appears to be very elastic and with the phenomenal margins enjoyed by packers the last number of years seems they can always find ways to accommodate all the hogs.

However the question that always hangs over the industry is “can you move the meat”. Export markets will be pivotal in maintaining profitability for pig farmers. This is something Canadian pork producers have understood for a very long time as 70% plus of our production needs to get eaten somewhere else. However now that American producers are into the same thing for 25% plus of their production, they’re becoming introduced to the concept. Geopolitical forces and trade disputes can leave producers in both countries “collateral damage” as the present noise between the US and China threatens.

I studied agricultural economics a long time ago and came to believe the maxim “that the market always clears at a price”. Then I got out in the real world where theory meets practice. Many of you although you don’t want to will remember 1998. I was brokering SEWs and feeder pigs at the time. At the end of the year some wag started a gallows humour joke. “ I took my 10 pigs to the sales barn. Went inside and when I came out there was 20 pigs in the truck”. Apparently the market doesn’t always clear! Or it does but unbelievably at a negative price.

Not suggesting we’re returning to anything like 1998 but as the whole North American industry now relies very heavily on exports it is very much in both countries producers interest to guard against protectionism and fight for open trade. Otherwise you can insert the word trade for sword in the old adage “live by the sword, die by the sword”

Hog profitability since my last commentary in the good, the bad and the ugly, has gone to the ugly. Here courtesy of Bob Hunsberger, Wallenstein Farm Supply. Projected profits currently for the next 12 months have fallen to $7.58 on average, but that is dependent on the present hog, corn and meal futures becoming reality. The present producer profitability levels ($45.82) per pig average production and ($27.25) per pig excellent production will certainly end the party if the present summer futures (or better) don’t soon become reality. The jungle telephone here in Ontario already suggests builders have had three proposed sow barns cancelled. Without a change in direction soon there will only be more.