EU and Spanish Pork Markets

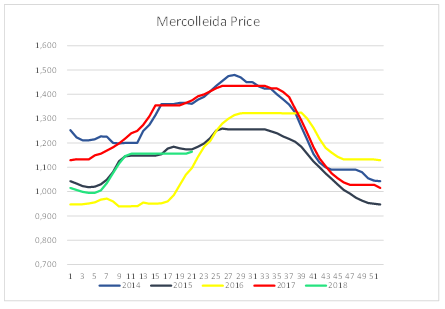

After 10 weeks of steady price at € 1,156 / kg live weight, this week we see a rise of € 0.008 / kg, reaching € 1,164 / kg live weight. The price curve of this year is similar to that of 2015. With an annual average of 1.20 compared to 1.21 and 1.10 compared to 1.11 respectively. 30 May 2018

30 May 2018

1 minute read

1 minute read

Mercedes Vega, General Director for Spain, Italy & Portugal, [email protected]

The year-on-year average with last year is almost similar €1.20 versus €1.24 in 2017, but the average so far this year is well below €1.10 versus €1.24.

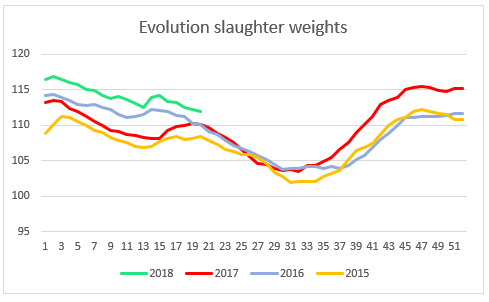

However, the weight is well above the weights of the last 4 years - 1.78 kg higher than a year ago, but more than 3.5 kg compared with 2015. The slaughter weight is increasing little by little. On the one hand because of market change - consumers looking for meat quality. On the other hand this helps to dilute the fixed costs of production. The future of prices is not very clear.

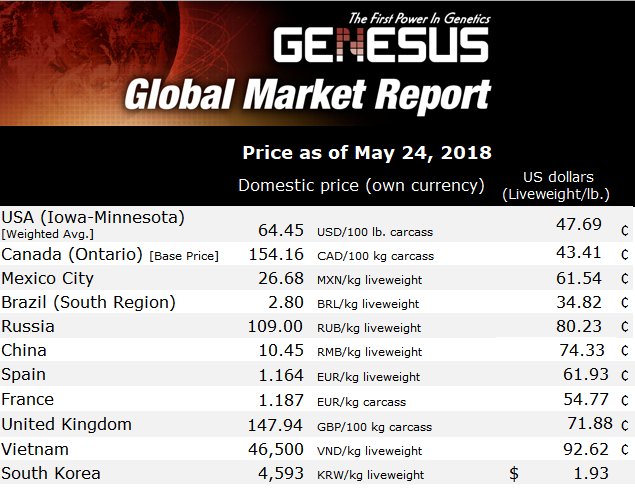

This does not happen in the rest of the EU. Where the weight is like a year ago or a little lower. However, the average price of Germany and Spain both, so far this year is at 1.10 -1.20 € / kg live weight.

There are fewer animals to sacrifice, less supply, but demand is accommodating to it. The price of meat prevents the industry from sacrificing more and maintaining its rate of slaughter so as not to worsen its exploitation account. However, the producer tries to compensate the price by keeping as much as possible the slaughter weight.

On the other hand the packing plant throughout the EU in general, does not want to freeze more meat than necessary. They do not see a very clear situation, which can cover the costs that this entails (current price, cost of conservation and future price).

In relation to exports, China has been buying 10% less in the first two months of the year to the EU, than in the same period of 2017. Regarding Spain exports, China and France are those that are first and second destination of exports. And although China represents 15% of exports, in relation to production it is 10%. These sales can be compensated, with a situation like the current one, with domestic sales within the EU, as in Eastern Europe or Japan and Korea.

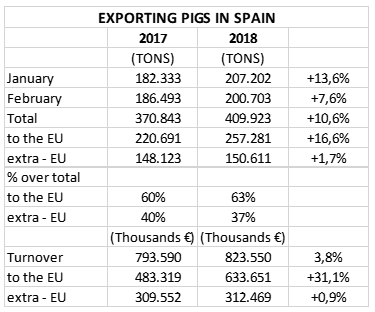

The following table shows how the first two months of the year exports increased by 10.6%, increased inter-community market compared to that of non-EU countries.