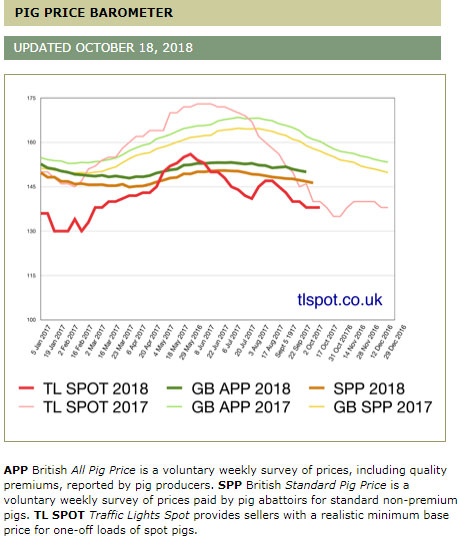

SPP continues downward track

Peter Crichton reports that although the SPP has continued its downward track losing another .42p to stand at 146.79p, thankfully EU mainland prices seem to have stabilised to some extent with the influential German producer price holding at 1.36 EUR which is equivalent to 119p in our money. 22 October 2018

22 October 2018

2 minute read

2 minute read

By:

By: Most weekly contribution prices have remained at similar levels within the 132-137p range but spot demand remains subdued with prices in and around the 140p mark but more for regular sellers.

A return of colder weather might help to boost retail demand and at the same time slow down the pigs growth rates and although there is something of a shortage of Freedom Food pigs in the system it will not be long before some of the major processors start to pull pigs forward for the Christmas period.

The Euro was traded on Friday at 87.83p which is slightly firmer than its value of 87.62p a week ago.

Cull sow prices have however remained at recent low levels with most worth in the 60-64p range according to load size but still well below their value of 78p this time last year.

Weaner prices have made up some of the ground lost last week with the latest AHDB 30kg average quoted at £52.16/head and 7kg piglets average at £37.55/head but once again this is very much a two tier market with Freedom Food contract pigs wanted but Red Tractor spot still hard to shift at almost any price.

Grain prices have ended the week at generally similar levels with London feed wheat quoted for November at £178.85/t and next May at £179/t. UK protein prices are also at similar stand on levels with 48% soya traded ex Liverpool at £324/t and 38% rape meal ex Kent at £207/t.

Chicago maize put in small gains due to reductions in predicted US maize production but soya bean futures fell due to forecasts of higher global rape seed production levels.

And finally, according to the latest June agricultural census there has been a 2% rise in the English pig herd compared with a 2% fall in the size of the Northern Irish herd and 3% less in Scotland.

Clean pig slaughter numbers have however been slightly higher than these results would suggest with 2% more pigs slaughtered during the July-September period.

Finished pig prices remained slightly ahead of COP piglets for the first half of this year but when the impact of more expensive feed and falling pig prices filters through producers viability levels will come under more pressure.

So it looks as though there will be more challenging times ahead, not to mention Brexit (which I just did) before a clearer picture of the profitability (or otherwise) of our industry becomes clearer as well as the potential impact of African Swine Fever which is now a very real threat to the whole of the EU pig industry.