It's time to rethink feed ingredient strategies

For many years, the US animal feed industry has relied on imports when it comes to micro ingredients. 21 September 2020

21 September 2020

1 minute read

1 minute read

By:

By:

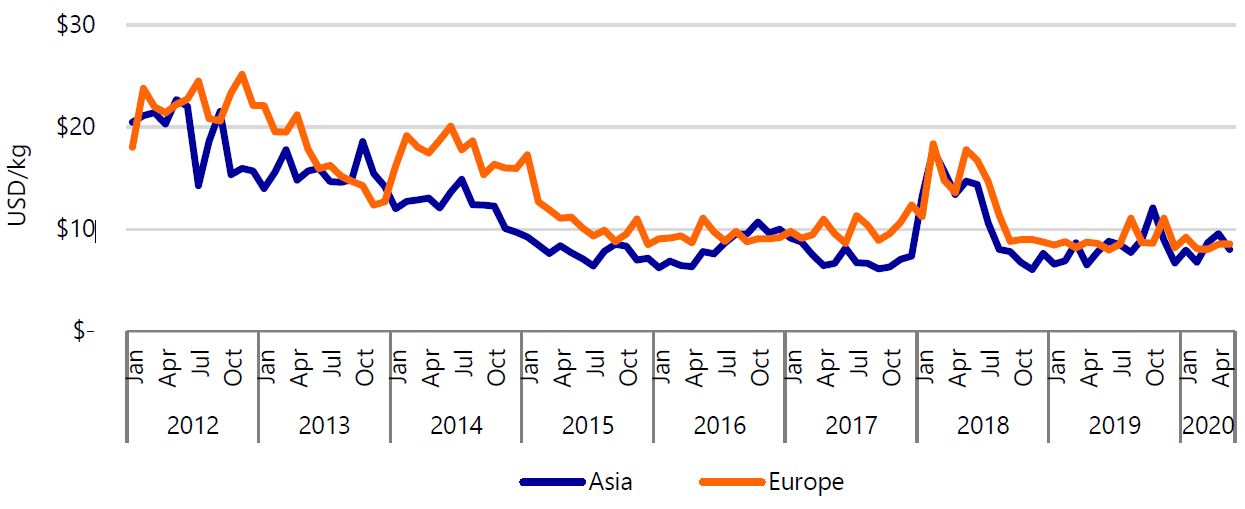

© U.S. Census Bureau, Rabobank 2020

© U.S. Census Bureau, Rabobank 2020