Weekly pig report: Disease pressure adds increased risk to hog supply outlook

Rising cases of PEDv and PRRSV are limiting herd expansion and reducing piglet survival, tightening future supplies and increasing volatility risk

25 April 2026

25 April 2026

6 minute read

6 minute read

By:

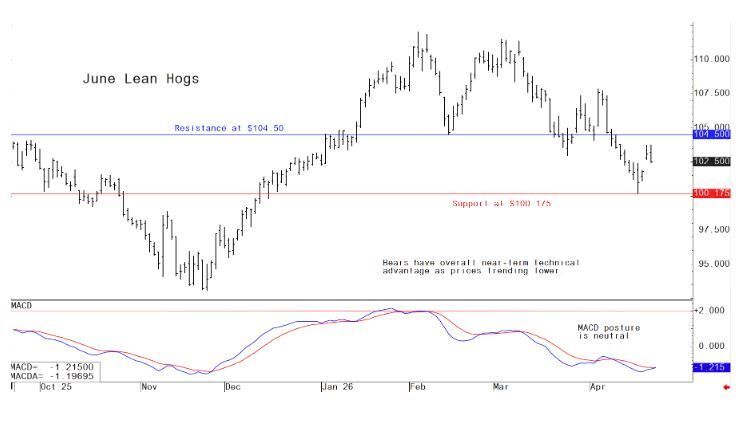

By: Lean hog futures price still in downtrend

June lean hogs on Wednesday fell $0.575 to $102.625. The hog futures market saw a corrective pullback from good gains posted Tuesday. Gains in hog futures were limited by selling pressure in the cattle futures. The latest CME lean hog index is up 14 cents at $90.51. Today’s projected cash index price is up 54 cents at $91.05. The national direct five-day rolling average cash hog price quote Wednesday was $70.75. June lean hog futures bears still have the overall near-term technical advantage. Prices are still trending down on the daily bar chart, which means the path of least resistance for prices remains steady to lower.

Pork Industry and related news

Weekly USDA US pork export sales

Pork: US net sales of 16,100 MT for 2026--a marketing-year low--were down 57 percent from the previous week and 60 percent from the prior 4-week average. Increases primarily for Mexico (8,900 MT, including decreases of 300 MT), South Korea (3,300 MT, including decreases of 400 MT), Colombia (3,300 MT, including decreases of 100 MT), Japan (1,600 MT, including decreases of 2,000 MT) and Canada (1,400 MT, including decreases of 300 MT), were offset by reductions for the Philippines (2,000 MT), Australia (1,900 MT) and New Zealand (600 MT). Exports of 38,200 MT were up 8 percent from the previous week and 2 percent from the prior 4-week average. The destinations were primarily to Mexico (17,300 MT), Japan (4,900 MT), South Korea (3,800 MT), China (3,600 MT) and Colombia (1,900 MT)

US hog Market sees seasonal tightening and disease risks

Elevated disease pressure and steady export demand suggest supply constraints could extend well beyond typical summer lows

Pork futures are already trading at a notable premium to seasonal norms heading into late April, and according to Zachary Davis of the NTG Morning Comments, the rally is being driven by both typical seasonal tightening and an increasingly important disease backdrop. As Davis explains, “the supply-demand math tilts bullish in a hurry,” with futures reflecting expectations that available hog supplies will shrink more meaningfully in the months ahead.

The seasonal pattern in the hog market is well established. Weekly hog slaughter typically peaks in March before declining into July as the spring pig crop moves through the system. That reduction in slaughter capacity is a key driver behind the annual rally in hog prices. While slaughter levels through mid-April have remained broadly in line with prior years, the expected seasonal downturn is imminent. Early signs are already appearing in the pork cutout, which has rebounded toward $100 per hundredweight after slipping into the mid-$90s earlier this month. A similar setup last year preceded a roughly $28 rally into early July.

What distinguishes this year from a typical seasonal move is the growing impact of disease within the hog herd. Porcine epidemic diarrhea virus (PEDv) positivity on sow farms surged to its highest level since 2022 earlier this winter, while porcine reproductive and respiratory syndrome virus (PRRSV) rates have climbed sharply on a year-over-year basis. PEDv is particularly disruptive because it kills the vast majority of infected newborn piglets, directly reducing future supply. Meanwhile, elevated PRRSV adds additional production stress, compounding losses across the system.

These pressures help explain why the US breeding herd has remained flat despite otherwise supportive price signals. Rather than expanding, producers appear to be replacing losses tied to disease outbreaks. The geographic spread of these issues — from the East Coast through the Midwest — underscores that this is not an isolated regional problem but a broader structural constraint on supply.

The result is a supply outlook that could tighten more aggressively — and for longer — than the market typically sees, Davis notes. Instead of bottoming out during the summer months, hog supplies could remain constrained into the fall, potentially extending through October. That shift would mark a meaningful departure from historical seasonal patterns.

Demand dynamics are reinforcing the bullish case. Export demand has remained steady, if not exceptional, providing a consistent floor for prices and limiting downside pressure. With no major weakness on the demand side, the combination of seasonal slaughter declines and disease-driven supply losses is skewing the market balance higher.

The key question now is whether futures prices have fully accounted for these risks. While the market has already moved higher, Davis suggests the current premium may still underestimate the extent of tightening ahead. If disease impacts continue to play out as current trends suggest, the rally in hog prices may have further room to run into the second half of the year.

China livestock sector on alert as new foot-and-mouth strain emerges

SAT1 detection across distant provinces raises containment concerns, triggers nationwide vaccine push

China’s livestock sector is moving into a heightened risk posture following the emergence of a new foot-and-mouth disease (FMD) serotype, SAT1, with early signals pointing to potential spread beyond initial outbreak zones. In early April, China’s Ministry of Agriculture and Rural Affairs confirmed the country’s first-ever cases of the SAT1 strain, detected on two farms in Xinjiang and Gansu — locations separated by more than 2,000 kilometers, immediately raising concerns about how widely the virus may already be circulating.

While authorities have not formally disclosed additional outbreaks, the policy response suggests mounting concern within the system. Emergency approvals have been granted to vaccine producers Zhongnong Weite Biotech and Jinyu Baoling, accelerating deployment of SAT1-specific doses.

Meanwhile, regional veterinary authorities are urging broad-based vaccination campaigns across cattle, sheep and swine populations — including in provinces far removed from the confirmed cases — signaling a precautionary nationwide containment strategy.

Market and industry behavior is reinforcing that view. The North China Livestock Trading Center in Hebei has already restricted live cattle shipments from affected and nearby regions, including Gansu and Inner Mongolia, according to reporting cited by Nikkei (link). At the farm level, producers report a sharp increase in biosecurity protocols, including tighter controls on farm access and animal movement.

Additional analysis from retired USDA economist Fred Gale underscores the uncertainty surrounding the outbreak and raises questions about the official narrative. Writing in his Dim Sums China agriculture blog (link), Gale described the simultaneous appearance of outbreaks thousands of kilometers apart as “implausible,” suggesting the virus may already be far more widespread than reported and that emergency vaccine deployment is a signal of broader transmission. He noted that current vaccines do not protect against the SAT1 serotype and that the disease likely entered China via contaminated people or equipment moving from Africa or the Middle East, where the strain has been circulating.

Gale also pointed to limited public disclosure and a lack of widespread official warnings to producers, drawing parallels to the early handling of the African swine fever outbreak in 2018. In that case, geographically dispersed early cases were followed by months of underreporting before the disease spread nationwide, ultimately cutting China’s hog herd roughly in half and sending pork prices to record highs.

There are, however, important differences. China has longstanding experience managing multiple FMD serotypes and appears to be acting more quickly with targeted vaccines and movement controls. The rapid authorization of SAT1 vaccines and early containment measures suggest authorities are attempting to avoid a repeat of the ASF scenario, even as outside analysts question how contained the outbreak truly is.

Even under a controlled-outbreak scenario, the economic implications are significant. Disease management — including potential culling — is likely to reduce China’s beef herd in the near term, with spillover risks to dairy and pork production. That comes at a time when many producers are already operating on thin margins, increasing the likelihood of supply tightening and price volatility across protein markets in 2026.

For global agriculture markets, the key question now is whether China’s early intervention can contain the outbreak — or whether SAT1 becomes another structural shock to the world’s largest livestock sector.

The next week’s likely high-low price trading ranges:

June lean hog futures--$100.175 to $105.00 and with a sideways-lower bias

July soybean meal futures--$308.90 to $328.00, and with a sideways bias

July corn futures--$4.55 to $4.75 and a sideways-higher bias

Latest analytical daily charts lean hog, soybean meal and corn futures