Weekly pig report: Mexico halts US hog imports amid New World screwworm concerns

After New World screwworm was recently discovered in the southern US, Mexico has suspended live animal imports, raising uncertainty for cross-border hog trade

13 June 2026

13 June 2026

6 minute read

6 minute read

By:

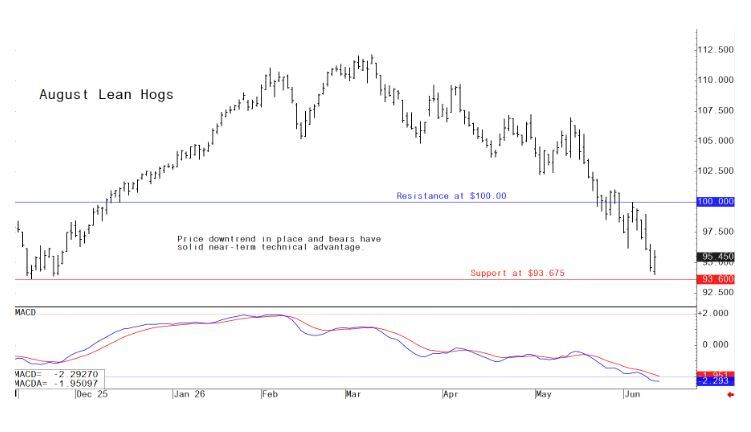

By: August lean hog futures on Wednesday rose $0.725 to $95.425 and hit a nearly seven-month low early on. The hog futures market saw some short covering and some perceived bargain buying. Near-term technicals remain firmly bearish as a price downtrend remains in place on the daily bar chart. A close on Friday near the weekly high would be one chart clue that the bears have run out of gas and that a near-term market bottom is in place. The latest CME lean hog index is up 13 cents at $92.76. Today’s projected cash index price is up another 16 cents at $92.92. The national direct five-day rolling average cash hog price quote Wednesday was $96.38.

Pork Industry and related news

Mexico halts imports of live US animals

Mexico's agriculture ministry said the country will halt most imports of live animals from the US after cases of New World screwworm were confirmed in Texas and New Mexico, Reuters reported. The suspension applies to cattle, horses, pigs, sheep, goats and several other species of animals, the ministry said, adding that the decision was made in coordination with USDA. The report said Mexico, which has seen over 28,000 cases of NWS since November 2024, cited the need to protect its cattle herd in the northern states of Baja California, Baja California Sur, Chihuahua and Sinaloa, where there are no current confirmed cases of screwworm.

China shifts livestock policy toward efficiency over expansion

Beijing’s new five-year plan prioritizes profitability, feed efficiency, and competitiveness as meat production growth slows

China's latest agricultural modernization plan signals a major shift in livestock policy, moving away from the rapid production growth that defined the past five years and toward a strategy centered on efficiency, profitability, and long-term competitiveness.

The 15th Five-Year Plan for Agricultural Modernization, released June 2, reflects lessons learned from a period of extraordinary livestock expansion. The previous plan targeted a 15% increase in annual meat production, from 77 million metric tons to 89 million metric tons by 2025. Chinese producers far exceeded that goal, pushing total meat production above 100 million metric tons last year.

While the surge strengthened domestic food supplies, it also created chronic oversupply across key livestock sectors. Pork and beef prices repeatedly fell to unprofitable levels as production outpaced consumption, forcing government intervention to stabilize markets and support producers.

The new plan takes a noticeably different approach. Rather than setting ambitious growth targets, Beijing now seeks to maintain annual meat production above 95 million metric tons. The target suggests policymakers are comfortable allowing production to retreat modestly from the record levels reached in 2025 if doing so improves industry profitability and market stability.

The pork sector remains at the center of China's livestock strategy. The plan calls for improved "production capacity regulation and control mechanisms" to keep pork supplies balanced and reduce the severe boom-and-bust cycles that have plagued the industry in recent years. Chinese officials appear increasingly focused on managing production levels to avoid the price collapses that have repeatedly hurt producers and required government intervention.

Beyond pork, the emphasis shifts away from expansion altogether. The plan highlights cost reduction, quality improvement, and efficiency gains across the broader livestock and poultry industries. The message from Beijing is that future success will be measured less by how much meat China produces and more by how efficiently and profitably it is produced.

One of the most significant elements of the plan for global agricultural markets is its continued focus on feed efficiency. China reaffirmed its goal of reducing feed usage by 7% on large-scale farms by 2030 compared to 2023 levels while maintaining production of meat, dairy, and eggs. The initiative is part of a broader effort to reduce dependence on imported feed ingredients and improve resource utilization throughout the livestock sector.

That development carries important implications for global grain and oilseed exporters. For decades, China's expanding livestock industry served as the primary engine of growth for world soybean demand. Massive imports of soybeans from Brazil, the United States, and Argentina helped support the country's rapidly growing pork, poultry, and aquaculture sectors.

The new plan suggests that era may be entering a more mature phase. If meat production stabilizes while feed efficiency improves, China's demand growth for soybeans and feed grains is likely to slow considerably. Over time, feed consumption could plateau or even decline despite stable levels of animal protein production.

For US agriculture, the plan reinforces a growing reality that China's role in global commodity markets is changing. Rather than being an ever-expanding source of feed demand, China increasingly appears focused on extracting more production from existing resources while reducing its reliance on imported inputs.

The strategy also has competitive implications. Beijing's emphasis on efficiency, quality, and cost reduction suggests China intends to strengthen the international competitiveness of its livestock sector. As production practices improve and costs decline, Chinese animal protein producers may become increasingly formidable competitors in regional and global markets.

Viewed through a broader policy lens, the livestock strategy is consistent with China's long-standing food security objectives. Beijing is not seeking to produce significantly more meat. Instead, it is trying to produce enough meat to ensure domestic food security while minimizing costs, improving profitability, reducing feed dependence, and enhancing the sector's global competitiveness.

For global agricultural markets, the takeaway is clear. The next chapter of China's livestock industry is likely to be defined not by rapid expansion but by optimization. That shift could moderate long-term growth in soybean and feed grain imports while creating a more efficient and competitive Chinese livestock sector capable of exerting greater influence on global protein markets.

Global food prices pause after three-month climb

FAO index slips in May as lower vegetable oil prices offset gains in cereals and sugar, but geopolitical and weather risks continue to threaten food inflation

Global food commodity prices edged slightly lower in May, ending a three-month streak of increases, according to the latest Food Price Index from the United Nations' Food and Agriculture Organization (FAO). The index slipped to 130.8 from 131.0 in April, reflecting what the agency described as a broadly stable global food market.

The modest decline was driven primarily by a 4.6% drop in vegetable oil prices, the first monthly decline for that category this year. Those losses offset higher prices for cereals and sugar, both of which posted notable gains during the month.

Despite the slight monthly easing, the FAO index remains 2.9% above its level a year ago, underscoring the persistent inflationary pressures facing global food markets.

Cereal prices rose 2.6% from April and are now nearly 5% higher than a year ago. The increase reflects growing concerns about weather-related production risks in key growing regions and ongoing uncertainty surrounding global grain supplies. Sugar prices surged 7.5% during May amid reports that a smaller share of Brazil's sugarcane crop will be directed toward sugar production, tightening export availability from the world's largest sugar producer.

Meat prices were essentially unchanged, rising just 0.1%, as weaker pork prices largely offset stronger beef values. The continued strength in beef markets reflects tight cattle supplies in several major exporting countries.

FAO officials cautioned that the apparent stability in food markets masks underlying vulnerabilities. Boubaker Ben-Belhassen, director of FAO's Markets and Trade Division, noted that rising cereal prices highlight the sensitivity of food markets to weather disruptions, energy costs, and agricultural input availability.

Particular attention is being paid to ongoing tensions in the Middle East and shipping disruptions affecting the Strait of Hormuz. Any prolonged interference with trade through the waterway could disrupt fertilizer shipments and increase energy costs, potentially raising production expenses for farmers worldwide and placing renewed upward pressure on food prices.

The May data suggest that global food inflation has stabilized rather than retreated. While lower vegetable oil prices provided temporary relief, rising grain and sugar costs, coupled with geopolitical uncertainty and weather concerns, indicate that food markets remain vulnerable to fresh price spikes during the second half of the year. For consumers and policymakers alike, the report serves as a reminder that food inflation risks remain elevated even as headline commodity indices appear relatively stable.

The next week’s likely high-low price trading ranges:

August lean hog futures--$92.00 to $100.00 and with a sideways-lower bias

July soybean meal futures--$300.00 to $315.00, and with a sideways bias

July corn futures--$4.10 to $4.35 and a sideways bias

Latest analytical daily charts lean hog, soybean meal and corn futures