Weekly pig report: Retail protein demand shifts in favor of pork products

Consumers trading down are boosting demand for affordable pork options like bacon and sausages, supporting overall value

1 May 2026

1 May 2026

4 minute read

4 minute read

By:

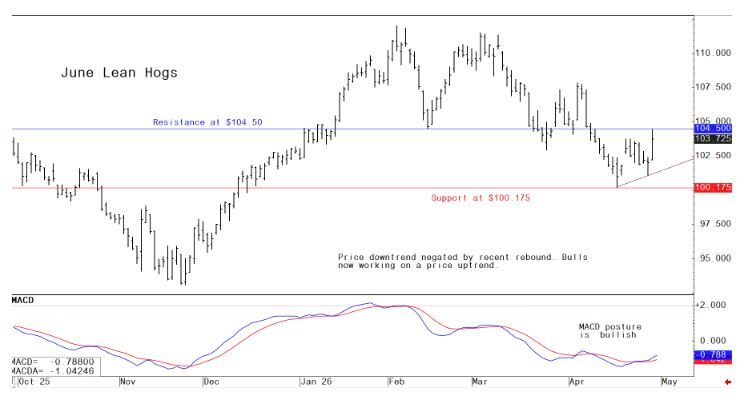

By: Lean hog futures prices rebound

June lean hogs on Wednesday rose $1.775 to $103.75 and hit a three-week high. The lean hog futures market saw more short covering and perceived bargain hunting. Strong gains in the cattle futures markets this week also supported buying interest in hog futures. The latest CME lean hog index is down 7 cents at $91.19. Thursday’s projected cash index price is up 12 cents at $91.31. The national direct five-day rolling average cash hog price quote Wednesday was $91.91.

Pork Industry and related news

China moves to stabilize pork market with state-backed purchases

Beijing leans on commercial reserves and local governments as hog prices weaken and supply pressures build

China’s agriculture ministry said Thursday it will support local governments in purchasing frozen pork for commercial reserves, a move aimed at stabilizing domestic hog prices amid mounting supply and demand imbalances.

The policy effectively expands Beijing’s long-running use of strategic and commercial pork stockpiles as a market management tool. By encouraging local authorities to step in as buyers of last resort, officials are attempting to put a floor under prices that have come under pressure due to ample hog supply and softer consumption trends.

China maintains both central government reserves and decentralized local reserves, which are periodically used to smooth volatility in the country’s pork market — a critical component of food inflation and broader economic stability. When prices fall too sharply, state-linked entities typically step in to purchase pork for storage; when prices spike, those reserves can be released back into the market to cool inflation.

The latest directive signals concern among policymakers that current price levels could undermine profitability across the hog sector, potentially triggering herd liquidation cycles that would tighten supply later and lead to renewed price spikes. That boom-bust dynamic has historically contributed to volatility in China’s food inflation, given pork’s outsized weight in the consumer basket.

Meanwhile, the intervention also reflects a broader effort by Beijing to stabilize rural incomes and agricultural production following a period of uneven recovery in domestic demand. Weak margins for hog producers have raised concerns about financial strain across smaller operations, particularly as feed costs and broader input prices remain elevated relative to recent years.

In global markets, China’s pork policy carries spillover implications for feed demand — particularly soybeans and corn — as herd size expectations influence import needs. If government support helps stabilize producer margins and slows herd contraction, it could underpin steadier demand for feed grains, offering some support to global agricultural markets already navigating geopolitical disruptions and trade uncertainty.

The move underscores how closely Chinese authorities continue to manage key food commodities, with pork remaining one of the most politically sensitive agricultural products due to its direct impact on consumer prices and social stability.

Weekly USDA US pork export sales

Pork: Net sales of 46,300 MT for 2026 were up noticeably from the previous week and up 34 percent from the prior 4-week average. Increases primarily for Mexico (26,100 MT, including decreases of 200 MT), China (8,800 MT, including decreases of 200 MT), Japan (3,600 MT, including decreases of 800 MT), South Korea (2,600 MT, including decreases of 200 MT), and Canada (1,200 MT, including decreases of 700 MT), were offset by reductions for New Zealand (100 MT). Exports of 35,000 MT were down 8 percent from the previous week and 6 percent from the prior 4-week average. The destinations were primarily to Mexico (16,300 MT), Japan (4,500 MT), South Korea (4,100 MT), China (3,000 MT), and Canada (1,600 MT)

Smithfield leans on packaged meats strength as earnings beat expectations

Private-label growth and at-home consumption trends underpin resilient consumer demand

Smithfield Foods reported first-quarter earnings that topped expectations on both sales and profits, pointing to steady demand for packaged meat products as a key driver and reaffirming its full-year outlook. The company highlighted strong performance across staple categories including bacon, ham, sausages, and hot dogs, as consumers continue shifting toward cooking at home to manage elevated food costs.

That shift in behavior — tied to persistent inflation pressures across grocery and dining — has reinforced demand for value-oriented protein options. Smithfield has responded by leaning into a dual-track strategy of premium branded products alongside a growing private-label portfolio, allowing it to capture a broader range of shoppers navigating tighter household budgets.

Private-label offerings have become an increasingly important pillar of the company’s retail business. As of its prior fiscal year, roughly 40% of Smithfield’s retail sales came from private-label products, reflecting a notable rise in “trade-down” behavior among consumers seeking lower-cost alternatives without exiting the category altogether. Rather than cutting back entirely on meat purchases, shoppers are substituting toward more affordable options — a dynamic that has helped sustain overall volume.

Meanwhile, consumer resilience has remained a defining theme. Despite broader macroeconomic uncertainty, demand for center-of-plate proteins has held up better than expected, particularly within grocery channels. Smithfield’s results suggest that while pricing sensitivity is shaping purchasing decisions, it has not materially eroded underlying consumption — instead redistributing demand across product tiers.

Looking ahead, the company’s maintained annual guidance signals confidence that these consumption patterns — at-home meal preparation, private-label expansion, and steady protein demand — will continue to support performance through the remainder of the year, even as economic conditions remain uneven.

The next week’s likely high-low price trading ranges:

June lean hog futures--$101.10 to $107.00 and with a sideways-higher bias

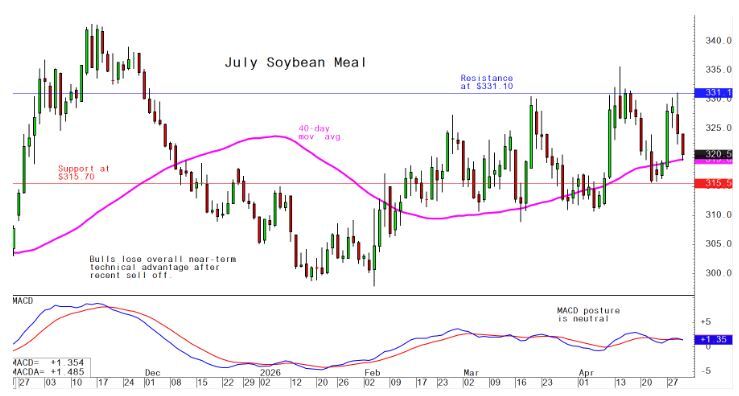

July soybean meal futures--$308.90 to $331.10, and with a sideways bias

July corn futures--$4.60 to $4.87 1/2 and a sideways bias

Latest analytical daily charts lean hog, soybean meal and corn futures\